Stephanie Rodriguez

Stephanie Rodriguez Craig Hurvitz

Craig Hurvitz

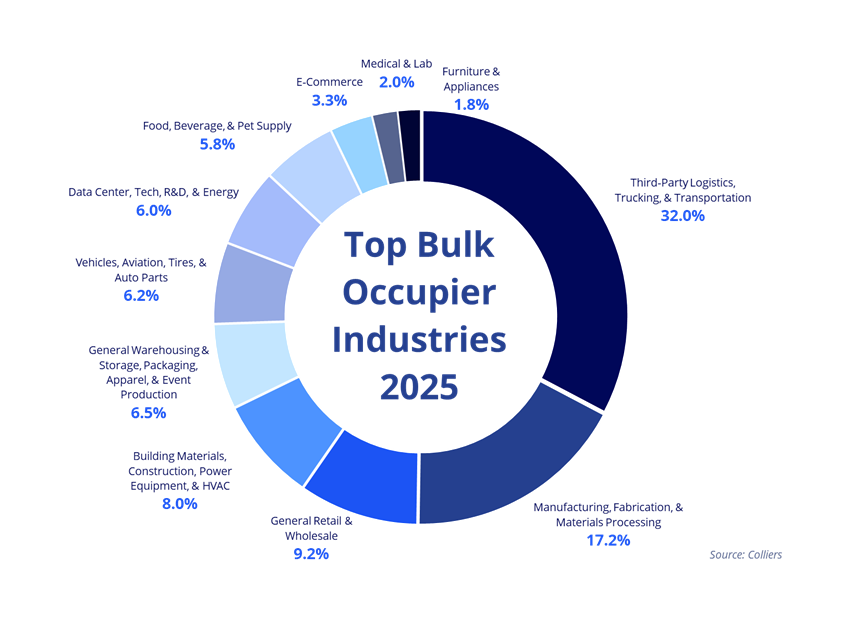

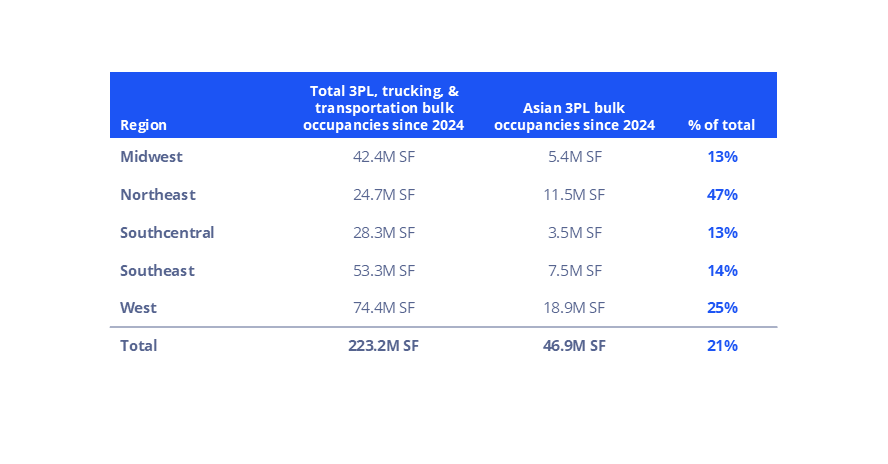

Asian-based third-party logistics (3PL) providers are rapidly expanding their presence across the U.S. industrial real estate market. Since 2024, 3PL, trucking, and transportation users have accounted for roughly one-third of bulk industrial occupancies (100,000+ SF), with Asian-based 3PLs representing 21% of that category. While their U.S. footprint was previously limited, these operators are now establishing a more meaningful foothold as they move closer to end consumers, reduce exposure to trade and tariff volatility, and strengthen supply chain resilience through proximity to key seaports and inland distribution hubs.

This expansion reflects a coordinated, multi-market strategy spanning West Coast port markets, inland logistics corridors in the Midwest and Southeast, and infill locations in dense Northeast and Southern California population centers. Driven by trade policy uncertainty, the need for greater control over end-to-end logistics, and sustained e-commerce demand, Asian-based 3PLs are localizing operations to enable faster delivery, diversify routing, and position inventory closer to consumers — signaling a long-term network buildout that is reshaping tenant demand and intensifying competition for well-located industrial space.

What’s Fueling the Expansion

Ongoing tariff volatility and shifting trade policies have pushed Asian logistics firms to establish a U.S. presence. By warehousing goods domestically, 3PLs can reduce exposure to policy risk, smooth cost fluctuations, and improve delivery reliability while limiting dependence on volatile international shipping.

At the same time, rising e-commerce expectations are making proximity to end users essential. Domestic distribution allows Asian-based 3PLs to meet faster delivery windows and offer greater reliability and improved service levels, while also aligning with reshoring and manufacturing hubs to support both inbound materials and outbound distribution, broadening demand beyond import-driven logistics.

Top U.S. Regions for Asian-based 3PL Providers

West Coast gateways continue to capture a large share of Asian-based 3PL industrial demand, particularly in port-centric markets like Greater Los Angeles. These locations remain critical first points of entry for trans-Pacific goods, allowing 3PLs to quickly deconsolidate shipments and push inventory inland. Strong intermodal connectivity and established logistics ecosystems make them essential for maintaining supply chain speed and flexibility.

Asian-based 3PL providers are also focusing on the Northeast, accounting for 47% of total 3PL bulk occupancies since 2024. In core industrial markets such as Northern New Jersey and Philadelphia, these firms have represented at least half of all 3PL bulk occupancies over that period. Proximity to the nation’s largest concentration of consumers, combined with dense transportation networks and port access, supports both regional distribution and last-mile delivery, while high barriers to entry and limited supply continue to intensify competition for well-located infill assets.

Beyond coastal hubs, Asian 3PLs are increasingly targeting key inland and Southeast markets, including Atlanta, Austin, Chicago, Cincinnati, and Savannah. These markets offer a strategic mix of central geographic positioning, access to major population centers, and proximity to growing manufacturing and distribution corridors. Robust highway and rail connectivity, coupled with relatively more cost-effective industrial space, is enabling these providers to scale operations efficiently. As a result, Asian-based 3PLs are building out integrated, multi-node networks across these regions to support faster delivery times, diversify routing options, and better align with evolving U.S. supply chain dynamics.

How Asian-based 3PLs Are Competing in the Industrial Market

Backed by large shipping and logistics conglomerates, many Asian-based 3PLs offer end-to-end solutions creating efficiencies that appeal to global shippers.

Advanced logistics platforms, automation, and data-driven inventory management give these operators an edge in speed, cost efficiency, and scalability. As these 3PLs expand, they are intensifying competition for large-format warehouse space, particularly in high-growth markets. This is reshaping tenant demand and putting pressure on both domestic and other international 3PL operators.

Implications for Industrial Landlords and Investors

Long-term leases from Asian-based 3PLs can provide diversity in the tenant mix for industrial assets, reducing reliance on any single industry or demand driver.

These 3PLs are poised to remain active— and increasingly entrenched — players in the U.S. industrial real estate market. Expansion is expected to continue in manufacturing-focused regions and major consumption corridors, with strategies evolving from opportunistic growth to long-term market integration. As these operators become permanent fixtures in industrial leasing, landlords and investors who understand their operational needs and risk profiles will be best positioned to capture this demand.

Nicole Larson

Nicole Larson