Aaron Jodka

Aaron Jodka

- Investors poured record venture capital (VC) funding into the life science industry in 2021. IPOs also set new highs.

- National Institutes of Health (NIH) funding is set to rise in fiscal year 2022.

- These factors are driving tremendous growth in both established life science hubs and numerous other markets.

- Research and development lab and cGMP manufacturing spaces are setting new pricing records as real estate investors clamor to get into this asset class.

- The future pipeline of new development is concentrated in Boston and the San Francisco Bay Area, suggesting that capital will continue to target the biggest markets in the U.S.

The life science industry shattered growth records in 2021. IPO numbers were off the charts, VC funding set new highs, and NIH grants increased, all creating unprecedented demand for life science properties. From research and development lab product to cGMP manufacturing spaces, tenant and investor demand has soared, mostly in the nation’s largest and most well-established life science hubs. Boston and the San Francisco Bay Area led the country in absorption, inventory, and VC funding, of which nearly 60% made its way to those two markets, per PitchBook. But other markets are aiming to make their mark as well.

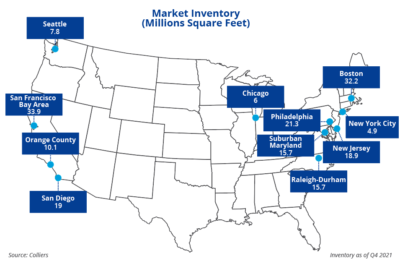

From a scale perspective, the San Francisco Bay Area and Boston rank first and second, respectively. The next tier is Philadelphia, San Diego, and New Jersey; Raleigh-Durham is its own tier, and other markets fall in line thereafter. Growth is happening in the Washington, D.C./Maryland market, as well as in Seattle, Chicago, and New York City. Other areas attracting life science growth include Boulder, Columbus, Houston, Los Angeles, Minneapolis, New Haven, Phoenix, and Pittsburgh, among others. Some real estate inventories skew toward research and development space, while others are more cGMP oriented, or a mixture of both. Medical device makers dominate markets such as Orange County, while plant science is a strength in St. Louis. Life science means different things to different investors: markets vary in product type, specialization, and sophistication.

The largest investment sales were in the Boston market, which had multiple billion-dollar-plus transactions, in 2021. Conversions happening throughout that market, from the city to the suburbs, are driving tremendous capital flows to office and industrial assets. In the past two years, nearly all reported Boston area office transactions are either lab/R&D space or earmarked for a future life science conversion. Conversions are taking place across the country, but the scale at which they are growing in Boston is second to none.

Advances in technology and science put drug discovery on a level never before seen. Early-to-mid-stage companies are scaling up and seeking bigger real estate footprints. Vacancies in most markets are incredibly low, many below 5%, indicating more space is needed for expanding tenants. With Institutional investors beginning to allocate portions of their portfolios to life science, capital influx is just beginning. As more product is completed, liquidity should only increase. Given the current scale of investment in Boston and the San Francisco Bay Area, along with their future development pipelines, they will continue to remain the most sought-after markets in the country.

Download the Quick Hits report.

Read more about the U.S. Life Science Report: First Quarter 2022 report.

Nicole Larson

Nicole Larson