Craig Hurvitz

Craig Hurvitz

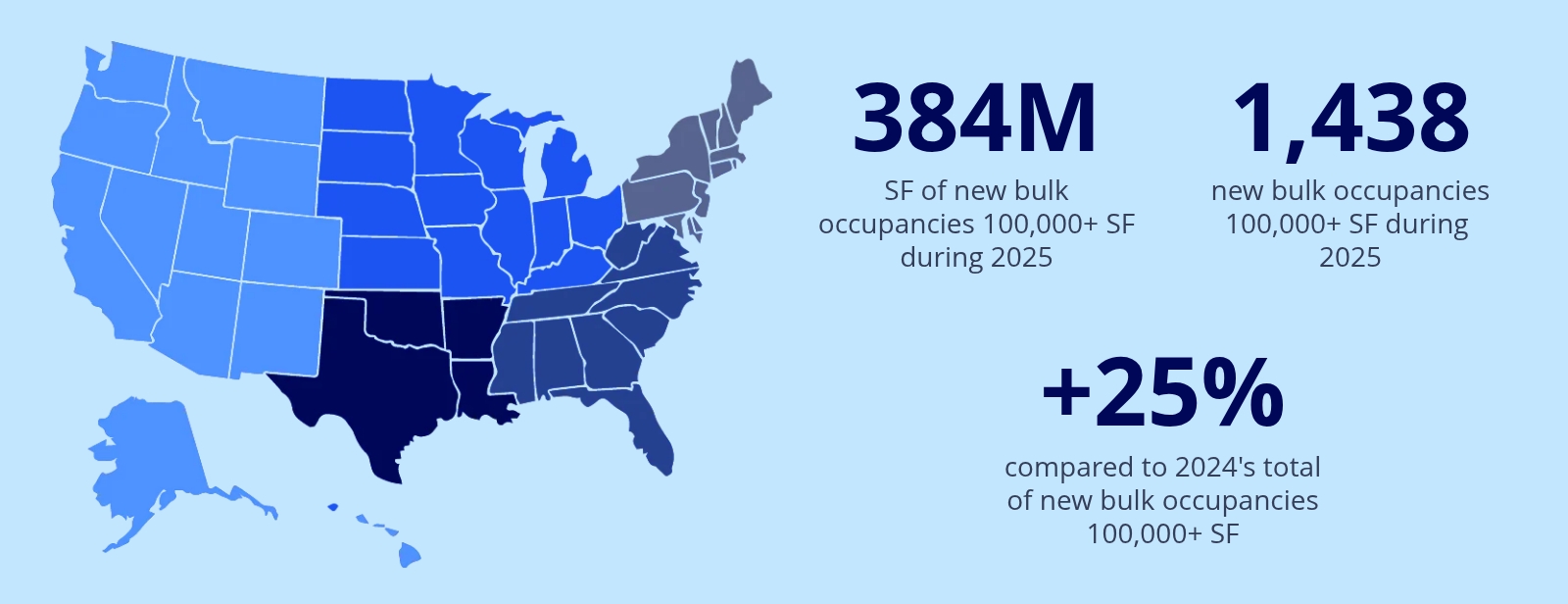

Stronger new leasing, build-to-suit completions, and user purchases pushed bulk industrial occupancies of 100,000 SF or larger to 384M SF in 2025, 25% higher than 307M SF in 2024. These move-ins also impacted net absorption, particularly in the second half of 2025, when demand more than doubled to 118M SF from 57M SF during the first half. However, move-outs remained elevated, offsetting the positive impact of growth in new bulk occupancies.

Users moved into 36 spaces of 1M SF or larger in 2025, more than one-third of which were build-to-suit facilities or user purchases. The largest new occupancies included Panasonic’s massive 4.7M SF electric vehicle battery manufacturing plant in Kansas, the 2.8M SF Ultium Cells battery facility developed by General Motors and LG Energy Solution in Michigan, and a 2.8M SF Samsung semiconductor facility in Texas.

The average bulk transaction size increased slightly from 2024 to 267,000 SF, but remained below the 2023 average of 289,000 SF and 2022’s 309,000 SF. Industrial users moved into more bulk spaces in 2025, with 1,438 spaces, up from 1,160 in 2024 and 1,041 in 2023.

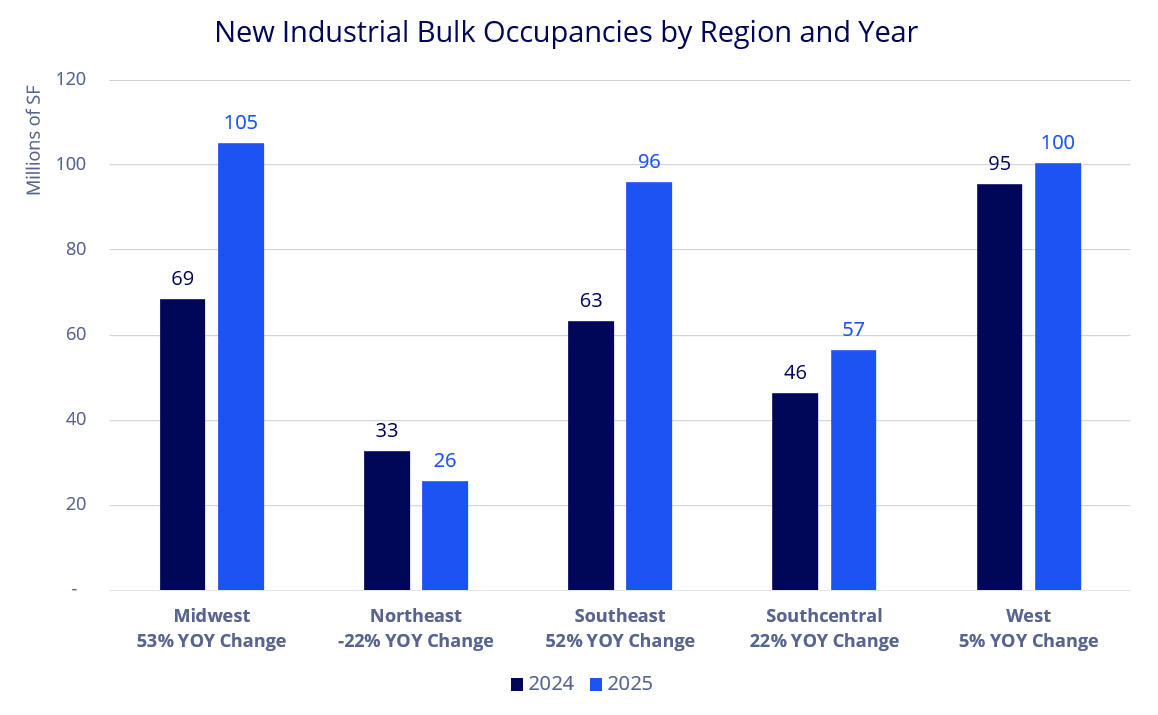

The greatest number of bulk occupancies in 2025 was in the West region, at 404 move-ins totaling 100M SF, up 5% year over year. The Midwest region had the greatest volume of bulk occupancies, 105M SF in 363 move-ins, 53% higher than in 2024, more than in any other region. The Northeast was the only region where bulk occupancies decreased year over year, down 22%, to 26M SF across 87 move-ins.

New occupancies increased in all size ranges in 2025, but grew the most in spaces between 500,000 SF and 749,999 SF, up 47% year over year. The greatest concentration was in spaces between 100,000 SF and 199,999 SF, with 792 move-ins totaling 108M SF, 23% higher than in 2024. The increase across all size ranges in 2025 is good news for the U.S. industrial market after a multi-year slowdown in bulk occupancies, especially in spaces 500,000 SF or larger, suggesting that demand for spaces both large and small is starting to build back.

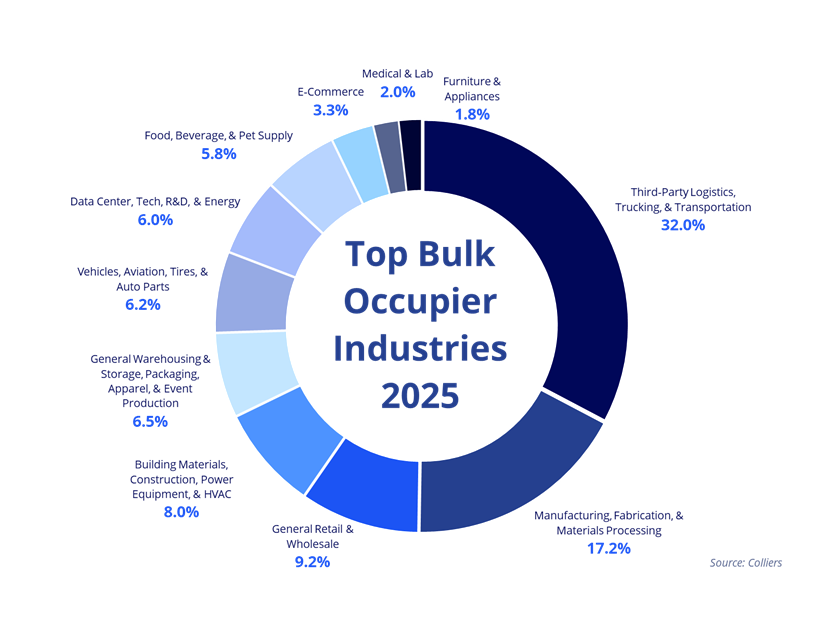

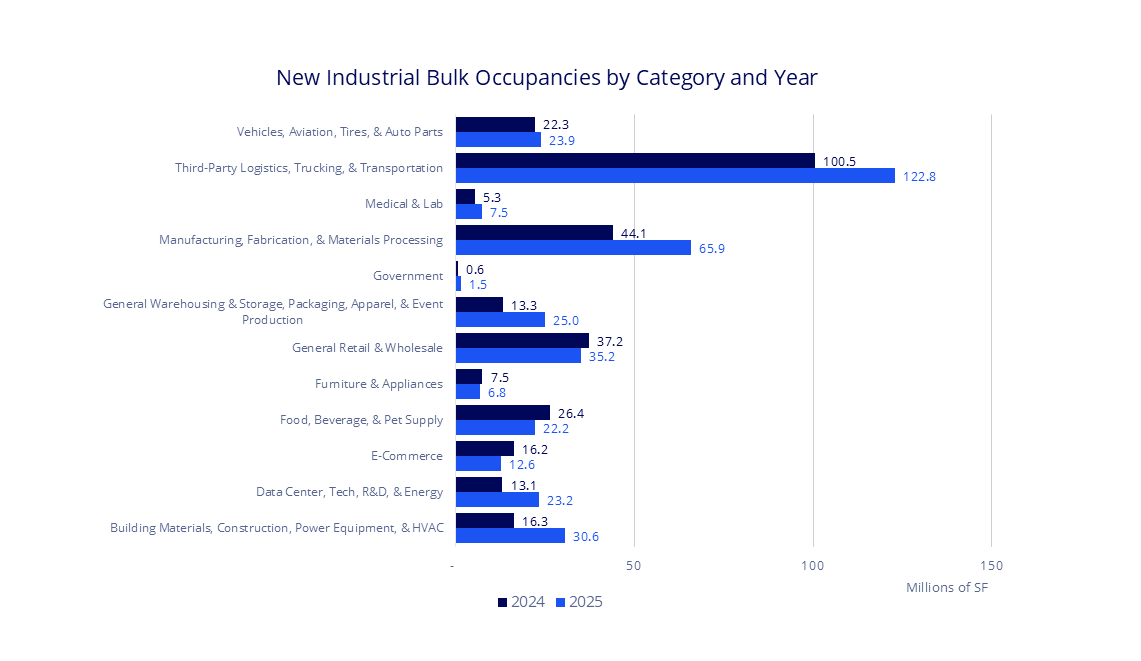

As in the past several years, third-party logistics providers, trucking, and transportation companies accounted for about one-third of bulk occupancies in 2025. These users moved into 123M SF in 430 occupancies, 22% higher than 2024’s 100.5M SF in 353 occupancies. This industry category was most prevalent in the Northeast region, accounting for 41% of all bulk occupancies in 2025.

Asian-based third-party logistics providers have continued to play a prominent role, accounting for 21% of all bulk occupancies in this category since 2024. They previously had small footprints in the U.S. but have become increasingly established to move closer to U.S. consumers, mitigate trade and tariff risks, and improve supply chain resilience by being closer to seaports and inland ports.

Manufacturing, fabrication, and materials processing companies moved into 66M SF of bulk space in 2025, 49% higher than 44M SF in 2024. More than 40% of those move-ins were in the Midwest region, where manufacturers occupied 27M SF in 2025. While manufacturing construction spending has slowed over the past year, reshoring demand will keep it higher than historical averages, even after the large-scale advanced manufacturing spurred by the 2022 CHIPS Act is completed.

E-commerce giant Amazon was the largest new occupier in 2025, moving into at least 20 bulk facilities totaling 9M SF. While the largest bulk occupier since 2020, Amazon has occupied less space every year since 2022. Mail and package courier DHL was the second largest, moving into 11 facilities totaling 6.8M SF.

Looking ahead, an uptick in new leasing over the past few quarters is expected to drive more growth in bulk occupancies in 2026 as users move into recently leased spaces and build-to-suit facilities are delivered. As the U.S. industrial market stabilizes and the construction pipeline bottoms out, new supply and demand are expected to return to equilibrium, and tenant move-outs will likely slow. This will result in a falling U.S. industrial vacancy rate after more than three years of increases, and new bulk occupancies will have a more significant impact on net absorption. As the market moves into recovery mode, some markets and regions will lead while others will lag, but the momentum created by a diverse set of industrial users in 2025 is expected to carry into 2026 and beyond.

Stephanie Rodriguez

Stephanie Rodriguez Matt Albertine

Matt Albertine Colin Alves

Colin Alves Pat Phillips

Pat Phillips Vincent Iadeluca

Vincent Iadeluca

Raul Saavedra

Raul Saavedra