Craig Hurvitz

Craig Hurvitz

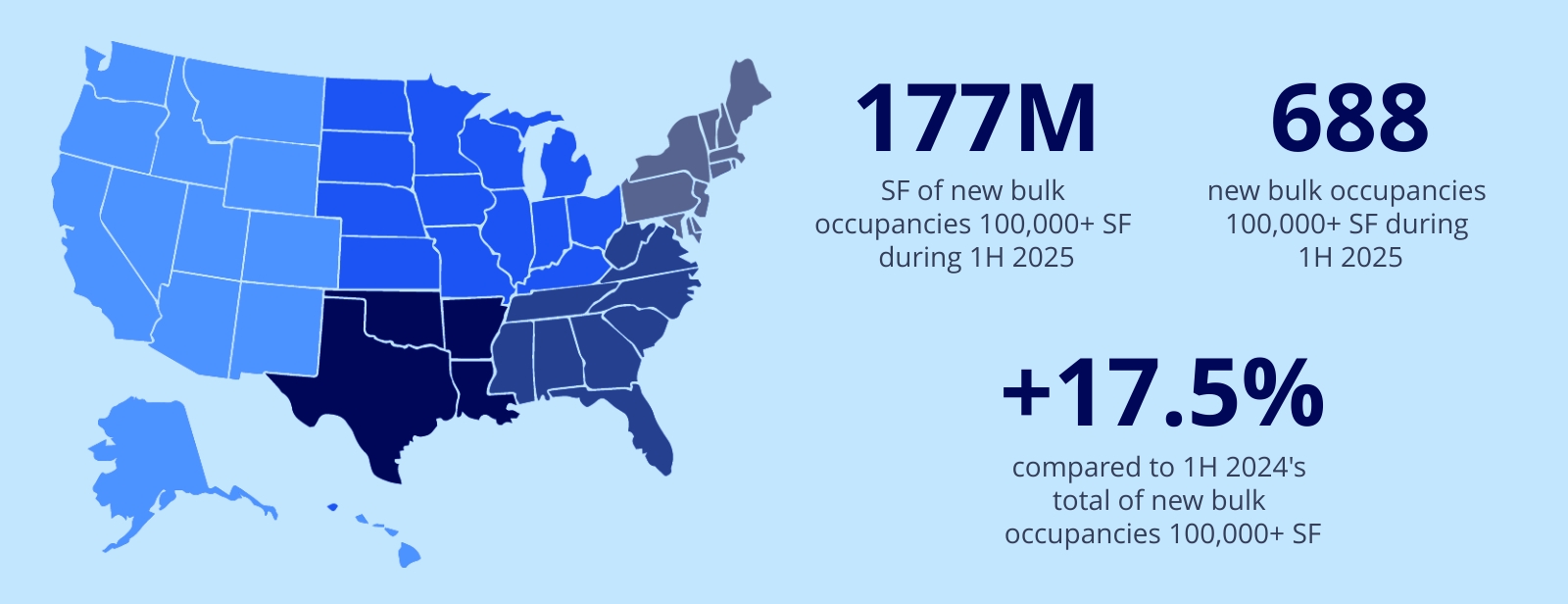

Move-ins, particularly in bulk spaces 100,000 SF or larger, were up in the first half of 2025. New industrial occupancies in that range, 177M SF during the first two quarters of the year, grew 17.5% from 151M SF during the same period in 2024. However, net absorption during the first half of 2025 of only 55M SF was 33% lower year over year. Move-outs increased as well, particularly in buildings smaller than 200,000 SF, offsetting the positive impact of these new bulk occupancies.

Fifteen new occupancies were 1M SF or larger, compared to 17 in the first half of 2024 and 19 in the first half of 2023. The average transaction size continued to decline, to 258,000 SF in the first half of 2025 from 264,000 SF in 2024, 289,000 SF in 2023, and 309,000 SF in 2022. While the average lease size is smaller, the overall number of bulk occupancies 100,000 SF and larger increased during the first half of 2025 compared to the same period in 2024 and 2023.

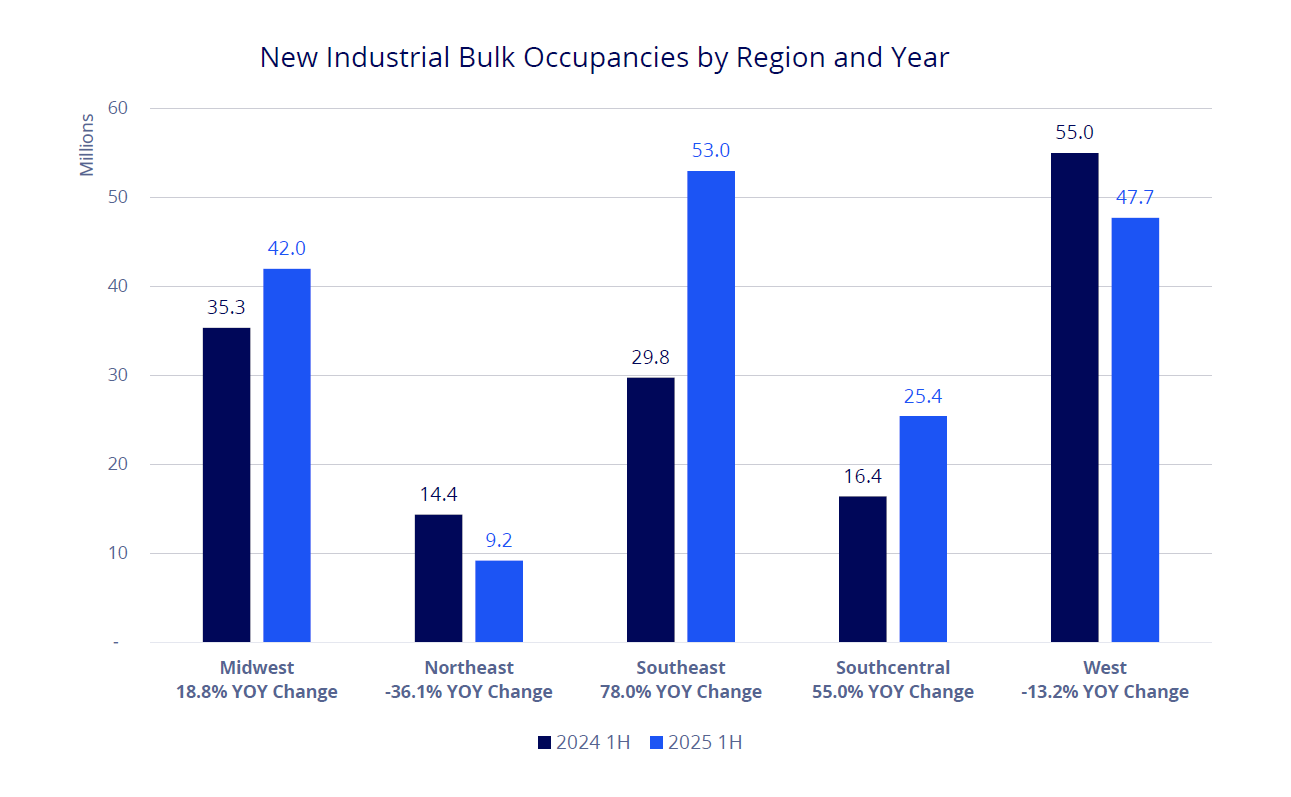

New bulk occupancies grew the most in the Southeast region year-over-year, as 204 users moved into 53M SF, more than in any other region, and 78% higher than the 30M SF in the first half of 2024. While bulk occupancies also grew year-over-year in the Midwest and Southcentral regions, they declined in the West and Northeast regions.

New occupancies increased in all size ranges year-over-year, but most significantly between 500,000 SF and 749,999 SF, where they grew 34% from those in the first half of 2024. While new occupancies in spaces between 100,000 SF and 199,999 SF increased 17% in the first half of 2025, net absorption in that range turned negative during that time because of an uptick in tenant move-outs. The year-over-year growth in all size ranges is an encouraging sign for the U.S. industrial market, suggesting tenant demand is starting to rebuild in spaces both large and small.

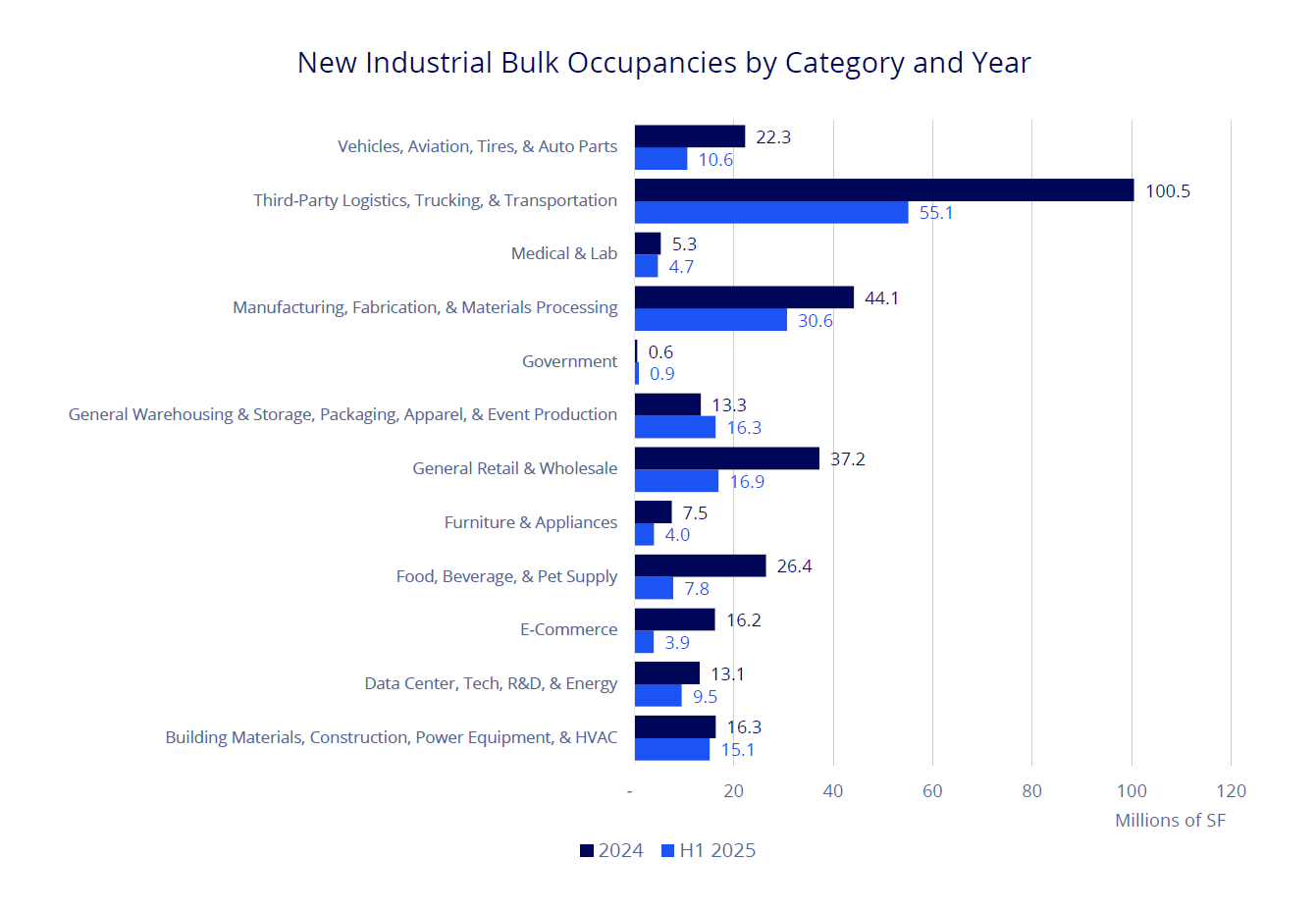

Third-party logistics providers, trucking, and transportation companies were the largest occupiers of new bulk space in the first half of 2025, at 31%. Since 2024, Asian-based third-party logistics companies have played a growing role in this category, occupying 21% of the total bulk space. While third-party logistics providers continue to drive leasing activity, they are also contributing to rising sublease availability, putting unused spaces on the market.

Manufacturing, fabrication, and materials processing companies held the second-largest share of new bulk occupancies, at 17%, slightly below their 19% share in the first half of 2024. While manufacturing construction spending has slowed year-over-year due to economic and trade policy uncertainty, bulk occupancies in this segment are expected to grow during the second half of the year, when several large-scale advanced manufacturing projects started in response to the 2022 CHIPS Act are expected to be delivered.

Top Bulk Occupiers in H1 2025

Electric vehicle manufacturer Tesla was the largest new occupier during the first half of 2025, moving into seven facilities totaling 3.5M SF in Nevada, Texas, California, and Illinois. Taiwanese semiconductor manufacturer TSMC was the largest new occupancy year-to-date, moving into nearly 1.6M SF in its new facility in Phoenix. Other mega-sized new occupancies included Tesla moving into a 1.5M SF facility in Sparks, Nevada; canned beverage manufacturer DrinkPAK moving into 1.4M SF in Fort Worth, Texas; and South Korean supply-chain management provider CJ Logistics moving into 1.4M SF in Stockton, CA.

Tenant demand is expected to increase again during the second half of 2025, led by third-party logistics providers, transportation companies, and manufacturers. As the construction pipeline continues to shrink over the coming quarters, new supply and tenant demand are expected to return to balance, and the U.S. average vacancy rate will peak. However, vacancy will climb higher in some markets than in others due to a pullback in demand and supply-side pressure, resulting in a segmented industrial market.

Don Moss

Don Moss