Colliers Insights Team

Colliers Insights Team

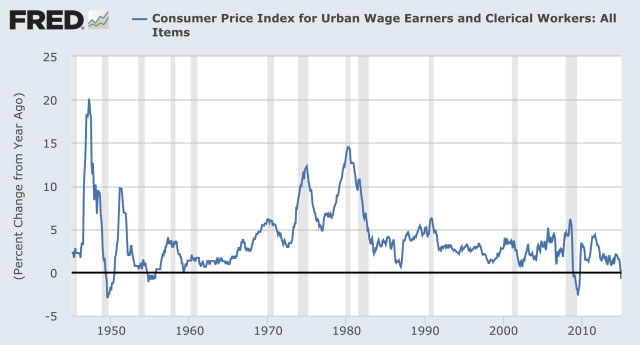

The Bureau of Labor Statistics recently posted the January 2015 Consumer Price Index (CPI) figures and the results show that the measure declined 0.1% from a year ago*. This would be of little consequence to most non-economists, but federal landlords must take note because the decline in CPI — for most GSA-leased properties — means a decline in rental income.

Also: Cutting the federal workforce | Who benefits from the surging U.S. dollar?

First, a little background on the CPI’s role in federal leasing: Most GSA leases — nearly all, in fact — include a clause that ties operating cost reimbursements to the change in CPI. This is one of those many GSA lease clauses that are foreign to property investors new to the federal sector. In GSA leases, an operating cost base is established based on budgeted operating expenses. But GSA does not reimburse actual cost increases above that base. GSA’s operating cost reimbursement (paid as “adjusted rent”) is calculated simply on the change in CPI. If, for example, your actual operating expenses increase 2 percent in a given year, but the CPI decreases 0.1 percent, you’re out of luck.

Plus: Is your rent-to-revenue ratio on target? | How experiential shopping ups the game for shoppers

(Federal Reserve Economic Data)

A 0.1 percent reduction computed on the operating cost base (which itself is only a portion of the full-service rent) causes a negligible rent reduction. So, why do we care? The reason is that the reduction highlights the disconnect between the government’s reimbursement method and the actual costs of operating commercial buildings.

The recent decline in CPI is driven primarily by the plummeting price of oil. The price of oil is a major component of CPI, and it also has pass-through effects on other elements of the CPI (for example, lower oil prices reduce the costs to produce and distribute other goods). However, oil price reductions don’t necessarily translate to operating cost reductions in commercial properties, primarily because their impact is largely indirect; oil is rarely used to generate the electricity that utilities provide to commercial buildings. Moreover, oil is also rarely used to heat commercial buildings. Though oil prices may drive down CPI — both directly and indirectly — they do not reduce building operating costs to the same degree. As a result, property owners must face dreaded “NOI leakage,” where costs increase faster than reimbursements.

According to an informal poll of our property management team, this appears — at least anecdotally — to be the case. Our Colliers Government Solutions team manages more than 40 properties leased by the federal government. We haven’t seen negative growth in operating costs nor are we budgeting for it.

This leads us to wonder how long CPI will remain in decline. So far, only the January CPI has decreased from the prior year. Therefore, rent reductions will occur only in those GSA leases with February anniversary dates (GSA establishes the CPI Index base as the month prior to the month of lease commencement). However, if history is any guide, the trend will ultimately affect most property owners. Since the end of World War II, there have been only three periods in which CPI declined year-over-year. All three periods were roughly a year in duration, suggesting that declining CPI could cause most GSA leases to suffer some reduction in net rent.

That said, this is a uniquely confusing time. And predictably, there is a lot of disagreement over whether we are really headed into a prolonged period of deflation or the CPI index is simply experiencing an oil price-induced blip on a path toward a healthier rate of inflation. In support of the latter argument, the Core CPI Index (net of energy and food prices) has remained positive. Further, there is now solid job growth in the United States, and the Fed is (so far) holding interest rates down in its quest to spur economic growth. On the other hand, CPI generally has been declining since the mid-1980s, wage growth is anemic, oil prices may stay low for some time and the strengthening dollar might actually hinder inflation.

Who really knows? All we can advise is that GSA-leased property owners watch their nickels and dimes this year.

*Throughout this article I refer specifically to the CPI-W (Consumer Price Index for Urban Wage Earners and Clerical Workers). The CPI-W is the CPI index utilized by GSA to calculate operating cost adjustments. The CPI-U (Consumer Price Index for all Urban Consumers) is more often cited by economists and the press. The CPI-U also decreased.

Kurt Stout is the national leader of Colliers International’s Government Solutions practice group, which provides government real estate services to private investors and federal agencies. He also writes about federal real estate on his Capitol Markets team blog. You can contact Kurt by email or on Twitter.