Colliers Insights Team

Colliers Insights Team

The financial markets seemed to breathe a deep sigh of relief this week. The VIX index of stock market volatility fell to its lowest point of the year and the major indices recorded their fourth consecutive weekly gain, while bond rates rose and the yield curve steepened. All of this seemed to suggest that we’re not about to fall into a recession after all.

There was never really much likelihood of that anyway. The market jitters that began just after the New Year with disappointing economic data out of China began to snowball out of proportion to the underlying economic reality. Despite some modestly negative economic news, the preponderance of domestic indicators remained at least mildly positive. And the leading indicators that economists look to did not suggest the economy was at a precipice.

In truth, economists generally were not nearly as worried as investors seemed to be, though risks clearly had elevated. But it wasn’t until the most recent economic data was reported in the last couple of weeks—the strong February jobs report and upgrade to January and December; the upward revision to 4Q15 GDP; and especially the rise in oil prices—that investors started to relax.

So, consider this vindication for my January blog urging confidence that the sky was not falling. At least for now.

But that still leaves the questions: Just why were the markets in such a funk? And should we have been concerned? At the onset, let us stipulate that explaining financial market movements always involves a high degree of speculation, no matter how definitive the narratives seem in the financial press, given the millions of investors involved.

But let us speculate nonetheless. There seems little doubt much of the recent market volatility and decline in share prices can be attributed to the fall in oil prices and the global economic slowdown. But why? One reason is that investors look to oil prices as indications of the strength of the global economy, and look at the global economy directly as a predictor of future U.S. growth. With both factors in decline, markets took that as signs of an imminent U.S. slowdown, or even recession.

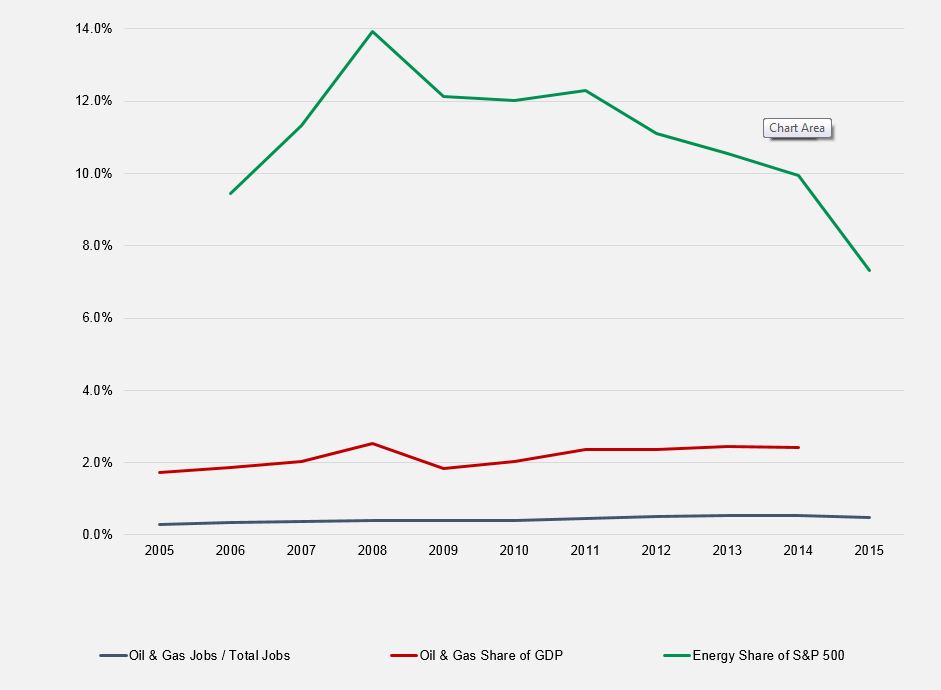

But there’s a deeper reason: These two parts of the economy mean a lot more to Wall St. than they do to the U.S. economy as a whole. The oil and gas sector accounts for only one half of 1% of U.S. jobs and 2% of the U.S. economy, as shown in the first chart below. So when oil prices fall, the negative impact on the economy overall is slight, though obviously more intense in oil-dependent regions. (Not to mention, there will be positive benefits to the economy from lower energy costs, yet to be fully realized, as consumers have more disposable income; transportation and manufacturing costs decline; and as a nation, we send less money abroad, particularly to countries we’d prefer not to support.)

By contrast, the energy sector accounts for 8% of the market capitalization in the S&P 500 – down from 14% in 2007, but still several times more than the sector’s share of our economy. So the energy sector has a much bigger impact on the equity markets, both directly and indirectly, than on the U.S. economy as a whole. Add to that concern about the exposure to energy sector loans among the big banks and it’s clear why the stock markets are so concerned with the price of oil, beyond its indication of global economic strength.

Oil & Gas Share of U.S. Economy and S&P 500

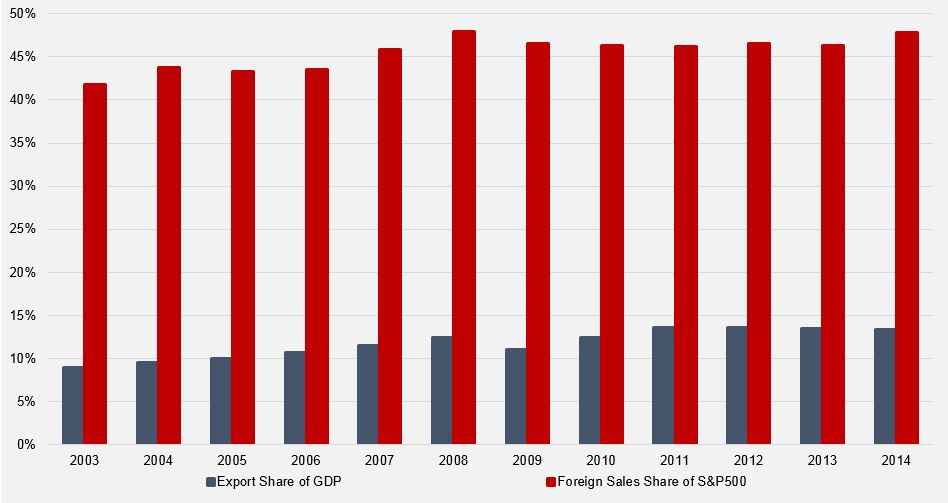

Similarly, the global economic slowdown is more important to the stock markets than to our economy as a whole. The U.S. is a relatively self-sufficient economy. In the second graph you can see that exports (in blue) account for about 13% of our economy. So when the global economy slows, it hurts us, but not that much. By contrast, the stock market is filled with global firms, and off-shore revenues (in red) account for almost half of the sales among firms in the S&P 500. So the sales and profit of these firms, and our equity markets, take a much bigger hit when the global economy slows compared to the U.S. economy.

Exports Share of GDP vs. Foreign Sales Share of S&P 500

In summary, it should be clear that financial markets are not reliable indicators of the state of the economy – there’s just too many disconnects between what floats stock prices and what drives our economy. But as bad as the markets are at gauging current economic strength, they’re even worse at predicting future economic trends. There have been more than 30 market corrections (a decline of at least 10%) in the S&P 500 since WWII, but only 11 recessions. In short, there’s too many false positives: stock market corrections falsely predict a future recession two out of three times.

All of which is to say, you really shouldn’t look to the stock market for indications on the economy. That insight should provide at least some comfort when stocks are dropping and your personal portfolio is getting pummeled: at least it doesn’t necessarily mean that a recession is at hand.

Of course, the longer market volatility continues, and the deeper the correction, the more worrying they become as the market jitters become a self-fulfilling prophesy: wealth, consumer business confidence all take a hit, leading to drops in consumer spending and business investment and ultimately economic growth. But those risks see remote for now. As noted, the volatility has already abated and the correction largely reversed. After being down as much as 12% from late December through mid February, the S&P500 is now virtually even for the year, as of this writing. Surely not enough to induce an economic slowdown by itself.

My advice when the financial markets start to rattle: Raise your antennas for signals about what the markets are really saying. And raise them higher still when we move into bear territory (down 20% or more). Caution is warranted. But remember that the financial markets consider many factors not central to the core economy, and need not suggest much about the health or direction of the economy itself. More often than not, it’s just the markets routine and healthy way of correcting excesses that have been building up in the system.

So relax.

Steig Seaward

Steig Seaward