Colliers Insights Team

Colliers Insights Team

“No, it’s not going to stop.” – Aimee Mann, Wise Up

Get ready for Black Friday. No, I don’t mean that you, as shoppers, should prepare your strategy to get the the best seasonal deals. Sure, shoppers willing to brave the sleep-deprived crowds early Friday morning will find some great deals – though dispassionate analysis of holiday shopping patterns demonstrates that the better deals generally are had by waiting until later in the season when retailers need to mark down their bloated inventories.

Rather, I mean, as real estate professionals, steel yourself for another another disappointing holiday season at the mall. Deloitte is expecting seasonal sales growth of 3.5% to 4% this year, ahead of inflation but below the 5.2% growth last year. But don’t expect the nation’s malls and department stores to see that growth. A disproportionate share of holiday sales will go to the humble discount stores, far away from the fancier shopping centers – no matter how full the parking lots seem next weekend. But the bigger story will be shoppers’ continuing collective flight to online shopping.

E-Commerce growing more slowly, but increasingly faster than in-store

One of the myths retailers and especially the shopping center industry tries to convince itself is that the shift to e-commerce is slowing. Newspapers and industry rags are filled with this wishful thinking. But even casual observation of shopping trends suggests otherwise. Just ask your teenager, or even your grandmother. They’ve already started their holiday shopping on their phones and tablets, from the comfort of their living rooms while they’re watching TV.

What folks in the physical retailing world like to highlight is that year-over-year sales growth in e-commerce is slower now than it was a decade ago, when online shopping was still in its infancy. Fair enough; in the middle of the last decade, e-commerce was growing almost 25% annually. Now the average growth rate has slowed to about 15% per year. Lower inflation accounts for some of the difference, but there’s no doubt that the real growth rate is lower now than it was before the recession.

Average Annualized Sales Growth Rates (Nominal Dollars)

| Online/ In-Store |

||||

| Total | In-Store | Online | ||

| 2003-07 | 6.3% | 5.8% | 24.3% | 4.2 |

| 2010-15 | 3.5% | 2.8% | 15.0% | 5.4 |

| Difference | -45.0% | -52.6% | -38.3% | +1.3 |

Sources: US Bureau of the Census, Colliers International

But physical retailers should take little comfort in this trend. Because here’s the thing: in-store growth has slowed even more on a relative basis. The annual in-store sales growth rate is now down 53% from before the recession, compared to 38% for online sales. Thus, online sales are growing even faster compared to in-store sales than they were previously – growing 5.4 times faster now compared to 4.2 times faster before.

Of course, e-commerce cannot sustain even this lower growth rate indefinitely, for at these rates e-commerce would surpass total retail sales in 25 years – logically impossible. So, yes, measured in this narrow way, online growth has slowed.

Growing online market share and the challenge to traditional retailing

But the more important metric is how much faster e-commerce is still growing than in-store sales, which is to say, how quickly online shopping is capturing market share from physical stores. And here the picture that emerges is much more of a challenge to traditional retailing.

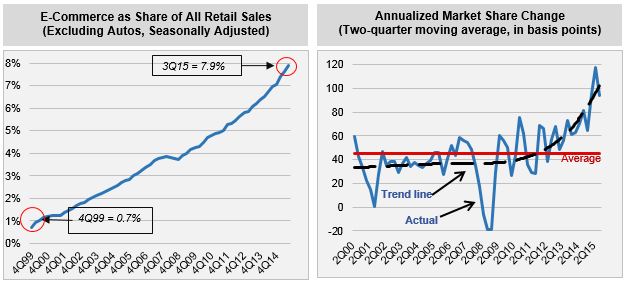

Online sales now account for 7.9% of total retail sales excluding autos, as shown in the left chart below, rising by an average of just under 50 basis points (bps) a year since the Census Bureau began tracking e-commerce sales in the fourth quarter of 1999.

Sources: US Bureau of the Census, Colliers International

Sources: US Bureau of the Census, Colliers International

Though the ascent appears relatively steady, in fact the online market share, while volatile, has been gaining momentum since the recession, especially recently, as shown in the right graph. In the three years prior to the recession (2005-07), the online market share rose an average of 45 bps per year. That is, the online market share was about 0.5 percentage points higher each year. This growth has surged by two-thirds during the last three years to an average of 76 bps, and to an annualized rate of 111 bps in 2015.

The reasons should be obvious: retailers are making online shopping easier and more compelling while shoppers are increasingly comfortable shopping online, facilitated by rising mobile payment options. As my colleague Anjee Solanki reported here last week, more people plan to shop on Cyber Monday than on Black Friday – a rather startling accomplishment for an event that started only ten years ago.

Clearly online sales cannot continue to grab market share trend indefinitely at this rate for the same reason that e-commerce could not continue to grow forever at double digit rates: online shopping soon would be larger than all retail sales. Again, logically impossible. Yet there is no reason to suspect retailing is anywhere near an inflection point of declining online sales growth. As noted, e-commerce still accounts for less than 10% of all sales (though far greater in some key categories such as electronics and books). And mobile shopping is really just getting started and has the potential to fuel even greater growth given the near ubiquity of smartphones.

And for holiday shopping, the challenges at the mall are even greater. Holiday shopping means gift shopping, shopping that in simpler times would transpire in department stores and at the mall, then increasingly at discount retailers, and now increasingly online.

Online shopping is especially for discretionary goods (the mainstay of malls)

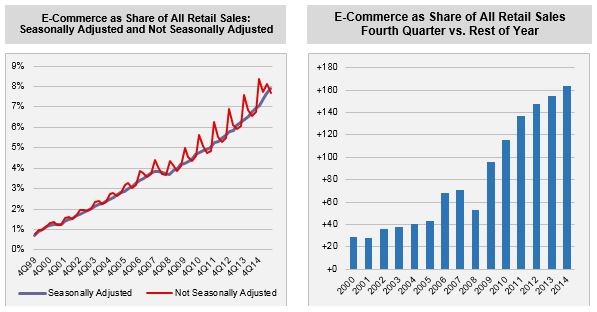

Definitive market share figures for online vs. in-store holiday shopping are not available, but we can get a sense of the trends by removing the seasonality smoothing from the quarterly sales figures, as shown by the red line in the left graph below. Those annual spikes represent the market share during the fourth quarter every year. And those spikes are getting larger over time, as shown clearly in the right graph. Last year, for example, the e-commerce market share averaged 6.7% during the first three quarters but jumped to 8.3% in the fourth quarter – a spike of more than 160 bps.

Sources: US Bureau of the Census, Colliers International

Sources: US Bureau of the Census, Colliers International

Thus, not only is the overall online market share still rising at an escalating rate, but the shift to online holiday shopping is growing even more so. Again, the reason should not be a mystery. Excluding autos, e-commerce has the greatest market penetration in discretionary shopping (such as apparel and hobbies) and the lowest share in convenience goods (groceries and personal care items). As the share of discretionary shopping surges in the fourth quarter, so too does the online market share. Malls are especially vulnerable to this sales erosion because they specialize in the kinds of goods most frequently sold online.

All of which means that malls and retailers without a winning omni-channel strategy are hemorrhaging sales during the all-important holiday season that are make or break for retailing. In the last few weeks we’ve seen all the department stores and many mall-based specialty chains report falling sales and downgraded forecasts.

It’s not for lack of overall retail sales. Even if growing more slowly, retail sales are now at new peak levels. And it’s not because more stores are splitting the sales. The size of the retail stock has barely budged since the recession, with less new construction – and less occupancy recovery – of any property sector. Instead, it’s the sales leakage to online shopping. And it’s showing no signs of slowing.

In the words of Aimee Mann, “no, it’s not going to stop.” And the shopping center owners and bricks-and-mortar retailers had best “wise up.”

Nicole Larson

Nicole Larson

Anjee Solanki

Anjee Solanki