Colliers Insights Team

Colliers Insights Team

At the end of each fiscal year, GSA produces an analysis of its leasing activity that provides an interesting glimpse into the federal real estate sector. This spreadsheet report, the Lease Turnover Analysis, seeks to address many of the questions lessors commonly ask about the probability that GSA will renew, vacate or even terminate leases. I imagine that GSA, tired of fielding endless calls from property owners, began publishing this analysis as a proactive measure to battle the onslaught of inquiry.

Plus: CPI has declined, and so has your rent | Cutting the federal workforce

That inquiry, of course, includes my own. Recently, I’ve spent some time reviewing the study and talking to GSA, and here are five observations:

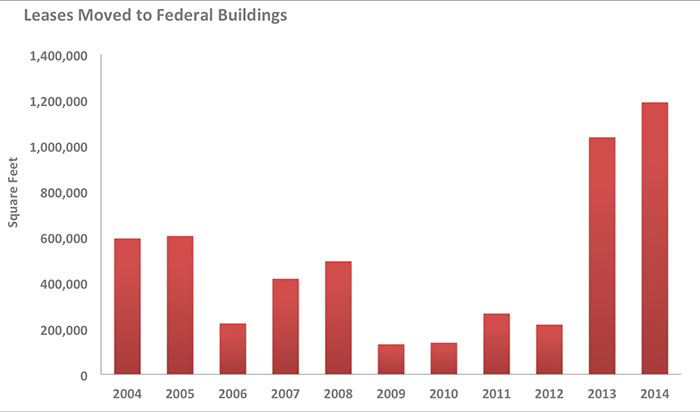

1. The shift into federally-owned space is no longer just talk

In each of the past two fiscal years, GSA has moved more than 1 million SF of leases into federal buildings. In the nine years prior — GSA tracks this stat back to FY 2014 — that figure averaged a little less than 350,000 SF.

One reason for the sudden increase probably relates back to the passage of the American Recovery and Reinvestment Act of 2009 (aka the Stimulus bill). GSA received $5.55 billion in Stimulus funds that were mostly used for building energy efficiency retrofits and renovations of federal buildings and courthouses. Now, many of those projects are completed, and they are pulling tenants in from leased space.

Also: Who benefits from the surging U.S. dollar? | U.S. office market outlook strongest since Recession

Another reason would be the 2005 Base Closure and Realignment (BRAC). The BRAC process resulted in an estimated increase of $35 billion in military spending to close bases across the United States and to build new federal facilities to accommodate the consolidated and realigned military structure. By law, the BRAC process was meant to be fully completed by September 2011. But as a practical matter, many of the affected Department of Defense-leased buildings were not completely vacated until 2013.

Both the Stimulus and BRAC are one-time or intermittent events. So, the pace of this shift to federally owned space could slow. Yet we expect it to persist so long as GSA receives improved funding for new construction and alterations as it has recently.

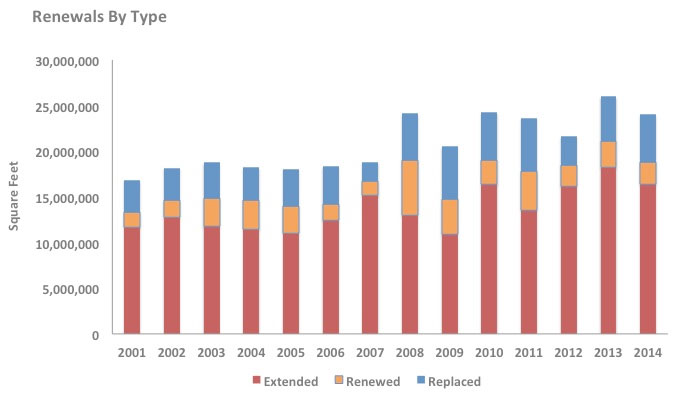

2. Most leases simply extend

It’s unusual that GSA lease extensions are far more common than new leases. In fact, lease extensions account for two-thirds of all of the GSA “renewals” across the inventory.

To understand this better, one must first recognize that GSA’s analysis categorizes are all “renewals” of three types: extended, renewed or replaced. By GSA’s definition, an extension is any lease action that extends the term of a current lease. This is done through some form of amendment, and it can include changes to other terms, too, including rent. A renewal in GSA parlance is meant to describe the specific instance where GSA exercises a previously contracted renewal option. Finally, a replacing lease is a new lease, written on a fresh lease form and provided with a new lease number.

GSA’s volume of lease extensions seems suspiciously high. But in an article last year I noted that much of GSA’s leasing activity has been lately comprised of short term extensions. Add to that long term extensions and perhaps the preponderance of lease extensions should not be surprising.

Going forward, we don’t expect much change. GSA is facing a huge pileup of lease expirations, such that one-fourth of all GSA leases expire in the next two years. GSA will struggle to manage the load and probably continue to extend leases as a strategic measure to work through the backlog.

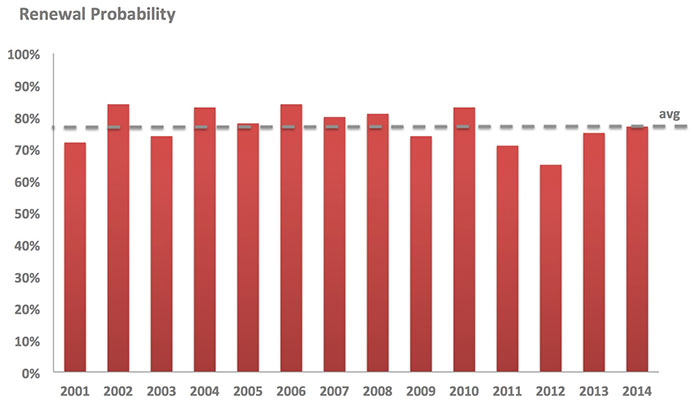

3. Renewal probability is lower than you’d expect — except that it really isn’t

To me, one of the most striking statistics in GSA’s study is the “renewal” probability — which we define here as the total of all leases where the government extended, exercised a renewal option or signed a replacing lease in the same building. For leases expiring in FY2014, the incidence of renewal was just 77 percent. In fact, in the 14 years GSA has performed this analysis, renewal probability, weighted by square footage, has averaged at about this figure, although it has ranged as low as 65 percent and as high as 84 percent.

The 77 percent renewal factor is deceiving because it represents the average for the entire portfolio. Therefore, it includes leases, for example, that are known to be subject to future consolidations. In those instances, renewal probability may be near zero. So, the likelihood of renewals in the remainder of the inventory would be much higher. Further, as we’ve often discussed with property investors, the probability of renewal in newer, purpose-built buildings is probably higher still.

Unfortunately, GSA’s study does not seek to explore renewal probabilities by tranche, but it’s a project that has been on our team’s backburner for quite a while. Maybe we’ll get to that this year.

4. Unexpected terminations are probably rare

In FY 2014, 1.3 percent of GSA leases were terminated during the soft term (as measured by square footage). Another 0.3 percent were terminated during the firm term, presumably through buyout negotiations or, possibly, default. We concern ourselves mostly with the former number as it reflects GSA’s propensity to exercise its termination rights.

A 1.3 percent rate of termination isn’t that high, but it seems a little more ominous when one considers that GSA is reporting the annual rate of termination. So, if your lease has five years of soft term that indicates a probability of termination closer to 6.5 percent (calculated roughly as 1.3 percent multiplied by 5 years). Figure also that about one-quarter of GSA’s leases have no termination right at all then. Using a back-of-the-envelope calculation, it’s starting to look like your lease could be exposed to almost a 9 percent probability of termination during its soft term.

However, as with renewal probability, looking only at the broad measure can be deceiving. This is primarily because most terminations are by design. For example, our team is working on three lease actions right now where we are expecting the government to terminate its lease and vacate. We have purposely provided a window of soft term in which the government can do that. In light of the fact that most terminations are expected — typically in the extended term at the end of a lease when it is in its final death throes — we can feel confident that unexpected terminations are very rare.

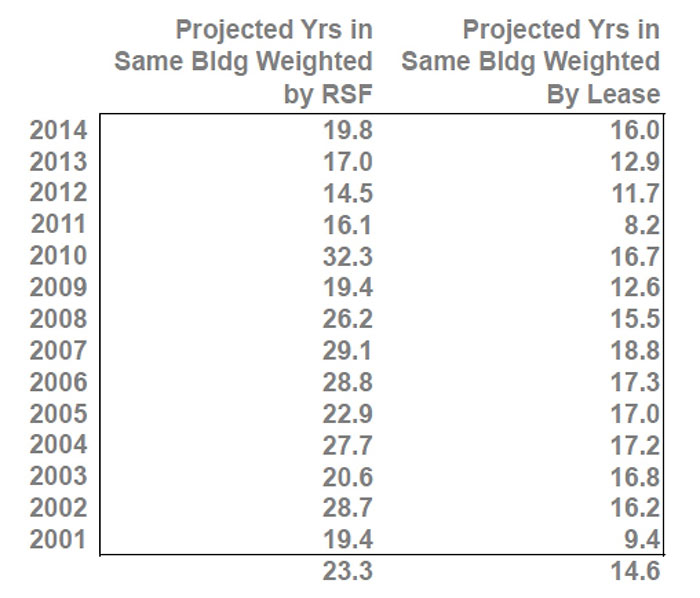

5. Big leases are “stickier”

For investors of GSA-leased properties, an intriguing section of GSA’s analysis is the table (recreated below) that projects the number of years GSA can be expected to remain in its leased buildings based upon the turnover probability in the year of analysis. As I’ve written about previously, turnover probability is not renewal probability. Rather, it is a figure that reflects the percentage of all leases in GSA’s inventory that remain active from one year to the next, regardless of their expiration dates. Normally, turnover in the GSA lease portfolio is 95 percent, plus or minus a couple percentage points. Using the turnover probability, one can project the anticipated number of years GSA will maintain its leased space.

GSA’s analysis concludes that its leases have an overall life of 14.6 years on average. Yet, when you weight turnover instead by square footage, that figure leaps to 23.3 years — although the projected years figure has been more subdued since the Global Financial Crisis. The obvious conclusion is that larger leases tend to stay in place longer. And we’d bet bigger leases in buildings predominantly leased and controlled by federal tenants are especially sticky. The implications of this tend to support the strategy of many of the fund buyers focused on purchasing federal properties for long-term stable cash flow.

Kurt Stout is the national leader of Colliers International’s Government Solutions practice group, which provides government real estate services to private investors and federal agencies. He also writes about federal real estate on his Capitol Markets team blog. You can contact Kurt by email or on Twitter.