Colliers Insights Team

Colliers Insights Team

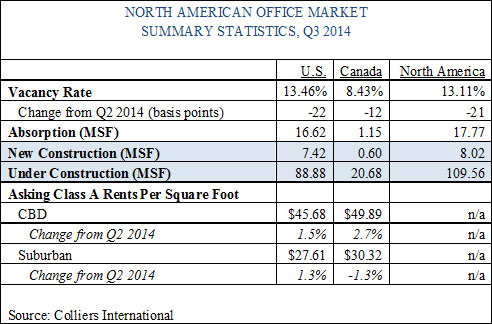

It was another solid performance for the North American office market in Q3 2014, with improvements in both the U.S. and Canadian markets. The U.S. vacancy rate was down another 22 basis points to 13.46%, the lowest level since Q2 2008. In a reversal of the trend in recent quarters, the Canadian vacancy rate also decreased, as the amount of new space coming on line slowed.

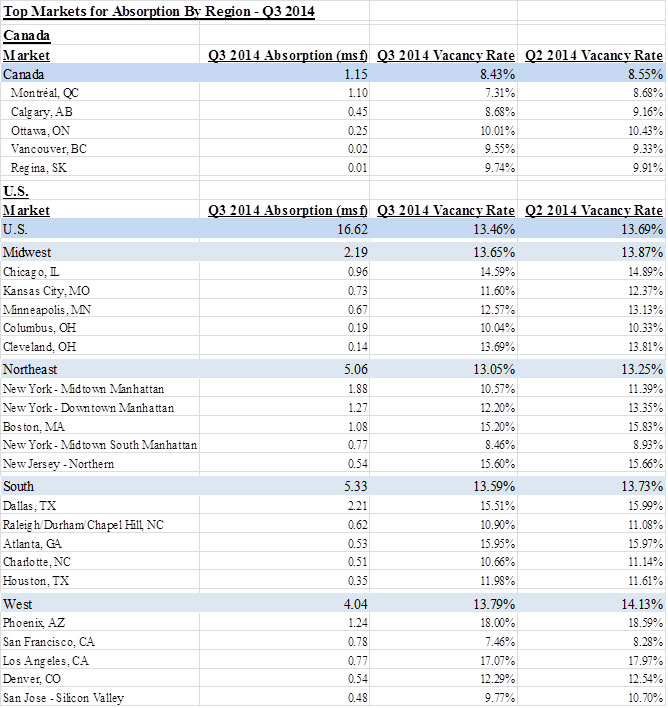

U.S. absorption totaled 16.6 million square feet (MSF) this quarter — the sixth straight quarter where absorption was above 14 MSF, and all but 19 of the 75 markets that Colliers tracks posted positive absorption. Dallas ranked first in quarterly absorption (2.2 MSF), followed by Midtown Manhattan (1.9 MSF), Downtown Manhattan (1.3 MSF) and Phoenix (1.2 MSF).

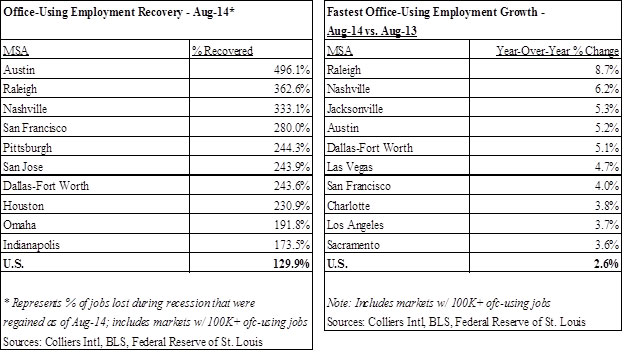

U.S. employers continued to add jobs in virtually every sector, including the key sectors for office demand: professional and business services, financial activities and information. In fact, as of August, the U.S. had recovered about 130% of the office-using jobs lost during the recession. Or, in other words, the economy added 1.3 office-using jobs for every one job lost during the recession. Office-using employment continues to track ahead of the recovery in overall employment; including all sectors, the U.S. economy has added 1.1 jobs added for every one lost during the recession.

Of the 82 U.S. metro areas tracked by Colliers, just 14 of those areas lost office-using jobs between August 2013 and August 2014. Also, more than half of the metro areas have recovered all of the office-using jobs lost during the recession. No longer is the list dominated by intellectual capital, energy and education (ICEE) markets; among the strongest markets for office-using job growth in August were Jacksonville, Las Vegas, Los Angeles, Sacramento, Orlando, Phoenix and the Inland Empire — metro areas that all were hit particularly hard by the housing and financial crises.

Office construction activity has been increasing in recent quarters as the market has improved, but overall activity remains low and focused on the strongest cities. The ratio of absorption to new supply, one of the key metrics we use to gauge the supply-demand balance of the CRE markets, was 2.2:1.0 in Q3 2014, indicating that office users absorbed more than twice the amount of space that was delivered to the market during the quarter. The top 10 North American office markets account for more than 60% of all office space under construction. A whopping 16% of North American office space under way is in Houston, where energy companies are scooping up large blocks of space at a rapid pace. More than one-quarter of North American office markets have no space underway, illustrating the measured approach to development that developers have taken during the current recovery.

For much more data and analysis on economic and office trends, please see Colliers’ soon-to-be-released Q3 2014 North American Office Outlook report.

Anjee Solanki

Anjee Solanki