Colliers Insights Team

Colliers Insights Team

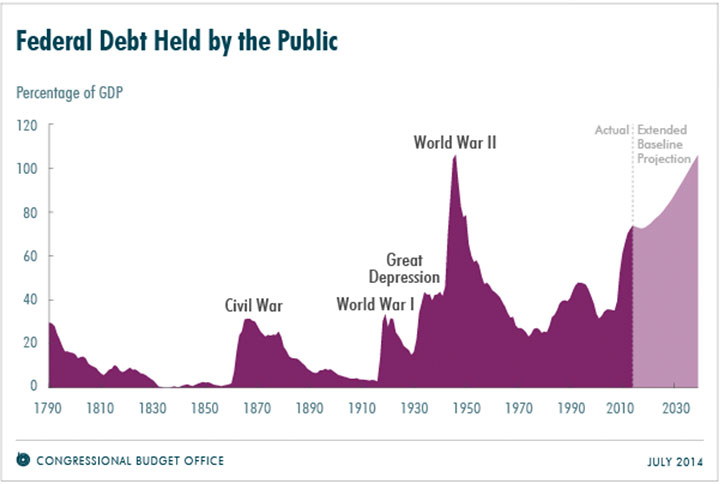

The federal debt held by the public in the second quarter of 2014 was $12.57 trillion. That equates to 72.6% of GDP, down slightly from the post-WWII peak of 74% that was recorded in the first quarter of this year. This slight reduction is the only good news that will be reported for the remainder of this article.

Rapidly rising U.S. debt is a problem for all of the reasons normally cited by economists. But for investors of federal government-leased properties, there is an additional cause for concern: Efforts to contain or reduce the growing debt through spending restrictions have come at the expense of the federal discretionary budget. Unfortunately, this is the same budget from which rent is paid.

In fact, we’ve already seen the early effects of these cuts. In response to historically high deficits and the resultant rapidly increasing debt, Congress and the White House have both begun imposing austerity measures on the federal inventory. The first of these were space utilization restrictions established by the House of Representatives as part of its prospectus approval process. Shortly thereafter, the White House issued its “Freeze the Footprint” policy, which prohibits agencies from increasing the size of their real estate inventories above the level established in FY 2012. Both of these measures have blunted GSA’s leased inventory growth and we are beginning to see downsizing in the works.

Much of this downsizing is being accomplished through reconfiguration of offices to achieve better space utilization. Occasionally, this is taken to the extreme, transforming workplaces into telework environments where most employees don’t come into the office. And those who do are provided temporary workspaces to conduct that day’s activities. The net result is that there is slightly less GSA-leased space now than a year ago.

The Heritage Foundation included this graph in its “Federal Spending By The Numbers” report last year, using data from the Congressional Budget Office (CBO) and the Office of Management and Budget (OMB) to forecast the squeeze put on the discretionary budget by entitlement spending and interest on the national debt.

Is this a temporary problem or a persistent one?

Ever optimistic, real estate investors hold out hope that the Ryan-Murray budget agreement and last year’s deficit reduction are signs that the economy is righting itself and that we will soon shift back into growth mode. Yet, that is unlikely.

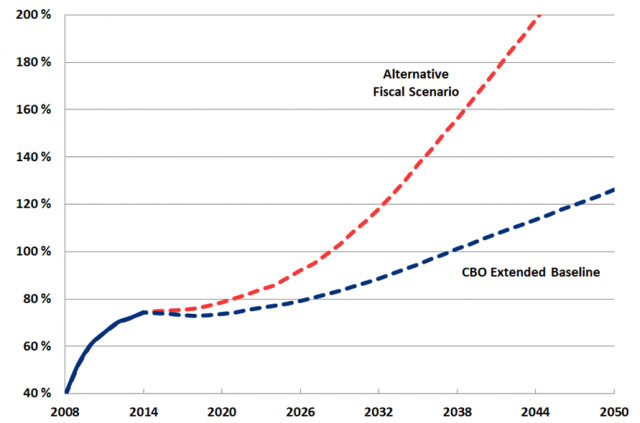

According to the Congressional Budget Office (CBO) Extended Baseline forecast, the national debt is expected to decline over the next few years, but then it will rise again (see chart below). The Extended Baseline estimate is CBO’s rosiest view of future debt because it is based on current law, which includes the expiration of certain tax breaks and Medicare reimbursements. In reality, those revenue-reducing provisions are consistently renewed. The Alternative Fiscal Scenario model, which is designed to consider past behavior in anticipating future results, yields a more worrisome trend. The most realistic forecast probably lies somewhere between these two measures, but, in any case, the results show that within the next 10 years debt will begin to grow again, exceeding current levels and ultimately surpassing the entire size of the U.S. economy.

From “The 2014 Long-Term Budget Outlook” published July 2014 by the Congressional Budget Office (CBO).

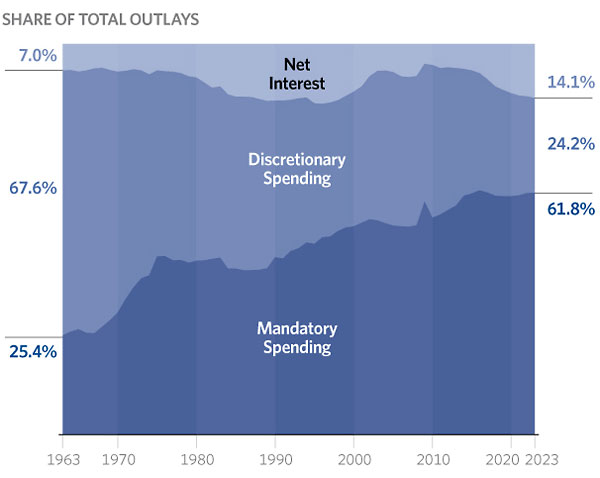

Both parties recognize that the root cause of ever-increasing debt is growth in entitlement spending (primarily Medicare, Medicaid and Social Security) and, to a lesser degree, increased net interest on the national debt. Currently, discretionary spending is a bit less than one-third of the federal budget, and mandatory spending (including net interest) is the other two-thirds. Although the Tea Party and other fiscal conservatives have waged relentless efforts to reduce discretionary spending, those gains toward debt reduction have been easily overwhelmed by entitlement spending. Part of the problem relates to lackluster GDP growth, which limits available revenues. But the big-picture math is pretty simple: Bringing the federal budget under control will require statutory changes to contain entitlement spending and/or increase taxes. Looking into the future, Fred Hiatt, Washington Post editorial editor, assessed the situation in an op-ed article in October: “The government will be spending on entitlement programs and interest alone just about what it spends today on the entire budget. Everything else — schools, pre-K, Pell grants, national parks, mass transit, housing subsidies — will get squeezed, or taxes will soar, or both.”

This is why we are unlikely to see a return to inventory growth anytime soon. Creating headroom in the discretionary budget is not possible without entitlement and tax reform, legislation requiring seemingly impossible congressional agreement in the current hyper-partisan political environment. Further, with a presidential election ahead in 2016, any legislative effort at deficit reduction is more likely to be a political statement than a real effort at compromise.

How can this get better?

The Ryan-Murray budget agreement was a two-year resolution. That provides about the most budget stability we’ve seen in the past several years. Further, it’s possible that the Republicans will capture both houses of Congress next month. If that occurs, the result for the federal-leased property market is likely to be positive simply because it consolidates control of the legislative branch with a single party. Split control of 112th and 113th Congress (Republican majority in the House and Democratic majority in the Senate) is a fairly rare circumstance, one that has manifest itself in legislative gridlock. The resulting state of limbo, paired with a slow and fragile economic recovery, has put agencies into a holding pattern, kicking the can with short term leases.

The irony for the feds is that intensifying budget pressure on leasing can be resolved through downsizing and consolidation, yet the budget is too tight to fund those activities. If the November midterm election unifies congressional control, it may provide a clearer path for agencies simply by providing greater predictability to the budgeting process. However, any improvement would be incremental; the government takes a shockingly long time to plan and execute even the simplest of leasing actions.

The trouble with rising debt cannot be enduringly addressed without landmark revisions to tax and spending legislation. Without action, it is a certainty that federal real estate will remain subject to cost-cutting. Property investors must hope that our future political leadership finds a solution to this important issue.

Kurt Stout is the national leader of Colliers International’s Government Solutions practice group, which provides government real estate services to private investors and federal agencies. He also writes about federal real estate on his Capitol Markets team blog. You can contact Kurt by email or on Twitter.

Coy Davidson

Coy Davidson