Colliers Insights Team

Colliers Insights Team

Over the last few months, many economists have been arguing that the U.S. economy has stabilized overall to the point that it would benefit from a hike in interest rates, allowing creditors to earn more while forcing borrowers of dollars to pay more for the privilege. So insistent have these arguments been, in fact, that many investment strategists and bankers believe that it’s not a matter of if but when in 2015 interest rates will rise – with some saying March 1, some May 1, some June 1 but no later.

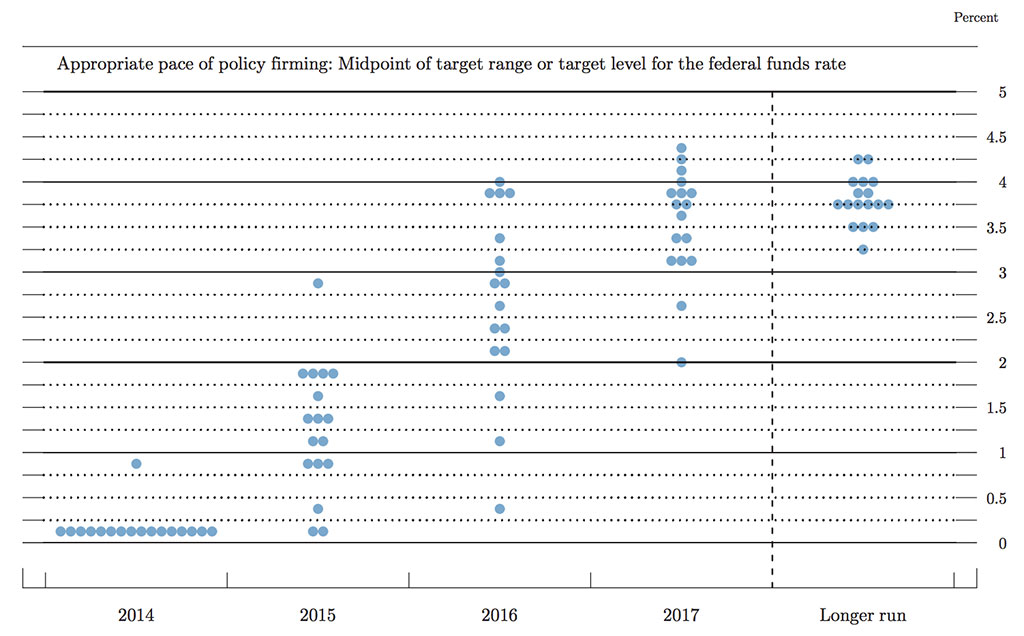

This chart, presented with the September 2014 meeting of the Federal Reserve Bank’s Federal Open Market Committee (FOMC), provides each member’s forecast of the federal funds rate. Each shaded circle indicates the value (rounded to the nearest 1/8 percentage point) of an individual member’s judgment of the midpoint of the appropriate target range for the federal funds rate or the appropriate target level for the federal funds rate at the end of the specified calendar year or over the longer run. (CapitolMarkets.com)

An early signal that this rise was imminent came in November, when, as the Washington Post reported, Federal Reserve Chair Janet Yellen and New York Fed President William Dudley both let slip that the Fed was preparing to raise rates off the zero-point floor that has been in place for the last six years, since the start of the Great Recession. “For the United States, the start of the normalization of U.S. monetary policy will be a very welcome development,” noted Dudley in his prepared remarks. Recognizing that the move might cause temporary turbulence in the financial markets, Dudley also argued that in the longer term a rise in interest rates would improve financial stability overall. Some economists note that that period of turbulence could result directly from a spike in the cost of the dollar in overseas markets, inhibiting a now healthy foreign exchange market. However, argued Philadelphia Fed President Charles Prosser, the zero-point floor is itself an agent of instability. “Raising rates sooner rather than later … reduces the chance that inflation will accelerate and require policy to become fairly aggressive with perhaps unsettling consequences,” he urged.

For all Yellen and Dudley’s signaling that rates may rise soon, the Fed has been careful in its approach. In its December meeting, it simply noted that its former insistence that rates would be kept at a zero floor for a “considerable period” would give way to the possibility of a policy change after patient consideration. Said Fed Chair Yellen, “The statement that the committee can be patient should be interpreted as meaning that it is unlikely to begin the normalization process for at least the next couple of meetings” — which means that any raise would probably not come before May 2015.

The markets responded favorably to the decision, although analysts are divided whether the 1.5 percent rise that followed the Fed meeting was an expression of relief that rates would not rise immediately or the beginnings of a run-up to be followed by a rollercoaster fall when the rise is announced. “Expect market volatility when the central bank drops its cautious tone as it paves the way for the first rate rise since the great recession,” noted the British paper The Guardian in its forecast for 2015, predicting that the ongoing uncertainty in the Eurozone and China will be to the dollar’s advantage.

The Fed predicts that 2015 will otherwise see moderate growth in the economy overall, fueled in part by lower gas prices, with little appreciable inflation and continued expansion in the job market. As for the bond market, the Financial Times encourages investors to be cautious in trying to time any move by the central bank to hike the interest rate. After all, it’s to be noted that, at this time last year, the smart money was on interest rates to rise in 2014 — and as 2014 enters history, rates have remained at historic lows, driven south by some unexpected hiccups in the economy last year. Even if the Fed raises the rate in 2015, most analysts believe that it will be only by a point or two.

It is beyond the scope of this blog to hazard a prediction as to whether the Federal Funds Rate will actually rise and when it may do so. It seems that every expert has been wrong on this at one time or another in recent years. Nonetheless, the chatter around this subject seems to be increasingly bullish on a rate hike next year. Regardless of what occurs, the anticipation of rising rates has been enough to influence the market for government-leased properties, especially those that are held as higher-yielding alternatives to long-term U.S. Treasuries.

With so much distress in the global and domestic capital markets, combined with ultra-low interest rates, the cap rate valuations of “safe haven” federal properties have benefited greatly, despite the fact that the underlying rents typically do not escalate through the term. Now the looming shift back to higher rates has property owners feeling a bit more urgency in their evaluation of whether to cash-in or to refinance. Some of this capital markets activity has already begun, and we expect this next year to be especially active both for investment sales and debt and equity placements.

Kurt Stout is the national leader of Colliers International’s Government Solutions practice group, which provides government real estate services to private investors and federal agencies. He also writes about federal real estate on his Capitol Markets team blog. You can contact Kurt by email or on Twitter.