Franklin Wallach

Franklin Wallach Verity Mosquera

Verity Mosquera

The Manhattan office market has been steadily marching toward a post-pandemic recovery. This was especially evident in 2024, as Manhattan’s office leasing volume – at 33.34M SF – was the strongest in five years, albeit still approximately one-fifth below 2019’s level of demand. On the supply side, the year ended with Manhattan’s availability rate at 16.5% – the tightest rate since September 2022 – driven by the strongest annual positive absorption in a decade (at 7.32M SF).[1]

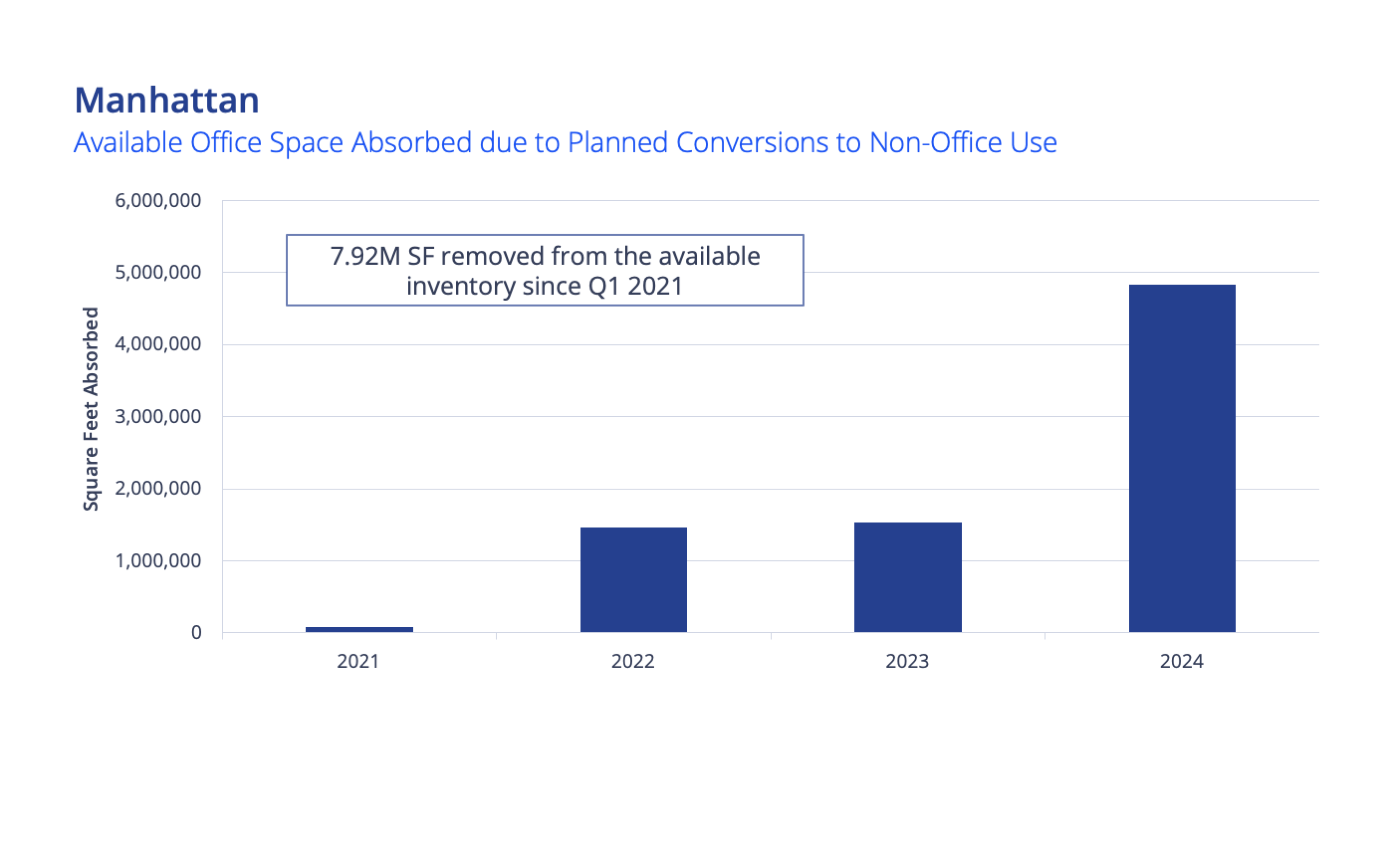

There is no question that the increased leasing volume played a significant role in 2024’s positive absorption with massive lease commitments (greater than 500,000 sq. ft.) from Citadel, Bloomberg, and The Blackstone Group along with a string of leases of countless sizes in almost every pocket of Manhattan. However, an even greater force impacting Manhattan’s tightening supply was the sheer number of announced conversions to non-office use (residential, hotel, storage, etc.) across the market. To illustrate, nearly 5.00M SF of office space was removed from the available inventory for planned conversion in 2024. This was more than three times the amount of available space removed for conversion in 2023 (1.54M SF) and 2022 (1.46M SF).

With millions of square feet of additional office inventory rumored for future conversion from office use, potentially accelerated by changes to New York City’s zoning laws, it’s important to examine the short-term and long-term impacts these office conversion projects could have on Manhattan’s future availability.

Short-Term Impact of Conversions

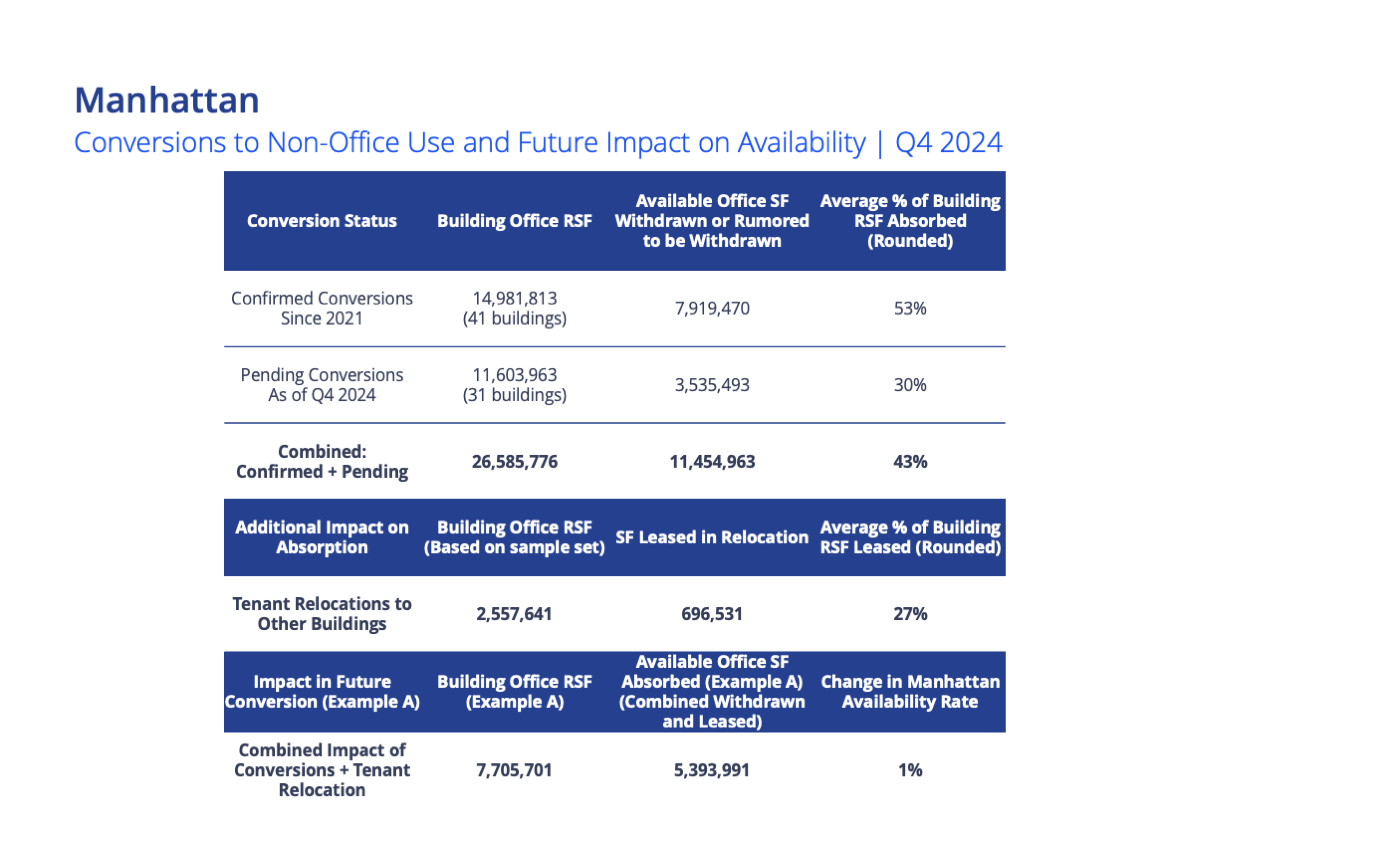

To understand the future impact of conversions on the market, we must first examine the immediate effect on Manhattan’s available supply of office space. To do that, we look at the conversions already announced along with the rumored conversions to identify certain trends. Over the last four years, 7.92M SF of available office space was withdrawn from the market within 43 buildings with a total RSF of 14.98M SF.[2] In addition, another 3.53M SF of available space could be withdrawn from the market across 31 buildings rumored to be under consideration for conversion totaling 11.60M RSF. Taken together a clear pattern emerges. On average, 43% of a building’s RSF is withdrawn from the market as soon as plans to change from office use are announced. For instance, if plans are later revealed to convert 20 buildings with a combined rentable square footage of 10.00M SF to non-office use, the market would immediately see approximately 4.30M SF of available space withdrawn from the available supply.

Long-Term Impact of Conversions

The impact of conversions on absorption and availability is not limited to immediate supply reduction. There’s also a long-term impact based on the additional tenant demand generated from these conversions. For instance, The Archdiocese of New York (relocation from 1011 First Avenue), the German American Chamber of Commerce (relocation from 80 Pine Street), Romano Law (relocation from 55 Broad Street) and Risk Strategies (relocation from 750 Third Avenue) are just a few examples of tenants who migrated within Manhattan from one office building to another due to an announced or planned shift away from office use. These relocations equal additional leasing volume in the market and a second round of absorption.

The level of absorption from this demand varies since not every tenant moving from an altered building relocates to the same footprint they previously occupied. Some might move to a different market or not sign a new lease at all for a host of possible reasons. Based on the prior relocation examples, the tenant demand seen in the market was equal to 27% of a converted building’s RSF. In other words, for every 1.00M RSF building scheduled for conversion, about 270,000 sq. ft. of additional absorption in the market will occur after these tenants sign leases and relocate. Altogether, the combined short-term and long-term impact of conversions means that, on average, a 1.00M SF building scheduled to transition to residential use could result in 700,000 sq. ft. of absorption in the Manhattan office market in what can now be called “the 70% rule.”

Future Conversions and Rezoning

The 70% rule can be applied to project how much absorption the Manhattan market might see from specific legislative initiatives. To illustrate, New York City and the State of New York have recently encouraged the conversion of underutilized office space through tax exemptions and rezoning to expand the City’s stock of residential units. One noteworthy program is 467-m, which provides tax incentives to landlords who convert non-residential buildings into rental housing.[3] An estimated 20,000 residential units could be built across New York City through this program.[4] The construction of 20,000 residential units is equal to removing roughly 26.00M RSF of office inventory from the market. However, these 20,000 residential units include all five boroughs (not just Manhattan) and likely include buildings that were already converted and factored into the positive absorption in recent years.

The exact square footage of office inventory that could be impacted by this program when adjusting for only the Manhattan CBD and removing already rumored or planned buildings is, therefore, difficult to pin-point. But for sake of argument, let’s revise using conservative estimates. First, if we suppose that 20%-25% of the planned units are outside of the Manhattan CBD, the 26.00M SF would be reduced to an estimated 20.00M SF. Next, if we presume that half of the buildings under consideration for conversion are already factored into the 467-m’s projections, then we would further revise the 20.00M SF down to an estimated 14.20M SF of Manhattan CBD office space.

Applying “the 70% rule” to the 14.20M SF of Manhattan office inventory that could be impacted by 467-m means that nearly 10.00M SF of absorption might occur in the short-term and long-term. Removing 10.00M SF from Manhattan’s 89.17M SF of office availability is not insignificant. All else being equal, the availability rate would drop from 16.5% to 14.7%. Of course, there is no guarantee that 10.00M SF would ultimately get absorbed. The eventual amount will depend on how many landlords take advantage of this program and how quickly these buildings get converted. Interestingly, “the 70% rule” could be used to reverse-engineer how many buildings would need to be altered to shift Manhattan’s availability rate by 1.0 percentage point. For instance, for Manhattan’s availability rate to tighten by 1.0 percentage point (equal to 5.40M SF out of a nearly 540.00M SF market), a total of 7.71M SF of building conversions would be needed.

Conclusion

The Manhattan office market’s gradual and protracted march towards recovery has been assisted by the higher tenant demand in recent quarters. Additionally, the planned conversion of millions of square feet of office inventory has also played a critical role in the form of a one-two punch to the supply. First, the space is withdrawn from the market in a building slated for conversion. Second, by generating additional leasing demand as tenants move out of the to be transformed buildings. Applying “the 70% rule” provides a comprehensive framework for estimating the potential impact of future conversions on market absorption. With zoning changes and incentives in place, the extent to which office conversions shape Manhattan’s future availability will depend on how aggressively landlords and policymakers pursue these opportunities.

[1] Note: Absorption quantifies how much available office space was removed from the market compared to how much space was added during the same period.

[2] Note: The available office space impacts Manhattan’s availability rate and is defined as any actively marketed direct or sublet office space available for tenant build out or possession within the next 12 months. Separately, the building RSF refers to the size of an office building and is a subtotal of Manhattan’s nearly 540.00M SF office inventory throughout Midtown, Midtown South and Downtown.

[3] Source: City of New York: https://www.nyc.gov/site/hpd/services-and-information/tax-incentives-467-m.page

[4] Source: New York YIMBY: https://newyorkyimby.com/2025/02/new-renderings-revealed-for-soma-office-to-residential-conversion-at-25-water-street-in-financial-district-manhattan.html

Marianne Skorupski

Marianne Skorupski

Anjee Solanki

Anjee Solanki Sheena Gohil

Sheena Gohil