Jeff Black

Jeff Black

- Upward pressure on property level debt is unlikely to change anytime soon.

- Continued interest rate volatility is causing headaches for levered buyers and property owners who need to refinance.

- Higher borrowing costs have made it challenging for buyers to generate attractive returns in most asset classes, and the ability to create positive leverage through debt has become rare.

- With rates rising, achievable leverage has come down significantly. Lenders are earning higher returns, while offering lower LTV loans.

- Lenders pursuing value-add bridge or construction loans are focused on their ability to exit in a high interest rate environment.

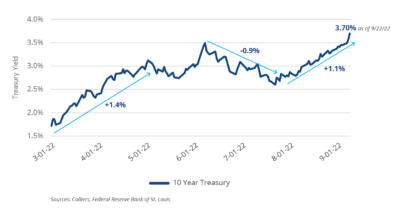

The debt markets have faced a yo-yo effect from Treasury rates that have been especially volatile of late. Rates on 10-year Treasuries rose 140 basis points from early March to early May, fell 90 basis points from mid-June to early August, and then reversed again, rising 110 basis points. As the Federal Reserve continues to increase interest rates to stem inflation (the overnight rate increased 75 basis points September 21), the upward pressure on rates will not change anytime soon.

10 Year Treasury Rate

With major money center banks becoming more conservative and increasing their cost of capital, local and regional banks filled in to provide liquidity at more favorable terms to borrowers. Given their balance sheets, local and regional banks can offer attractive terms and flexibility unavailable from the national groups.

Lenders are offering lower loan-to-value ratios, stemming from owners’ inability to cover debt service at higher interest rates. With higher borrowing costs, buyers are rarely able to find positive leverage, causing pricing to adjust or deals to be pulled from the market. Finding a new “normal” has been challenging. Opportunistic debt funds, however, also stand to benefit from the market dislocation. Debt funds are now able to win deals at higher returns and moderate leverage levels, with the ability to be more selective in their pursuits.

We anticipate that capital allocators and investment managers will ramp up their investment into credit strategies as the relative risk pendulum swings in favor of debt as a defensive strategy in a rising interest rate environment. A corollary effect of this trend is consolidation: global LPs (pension funds, sovereign wealth, etc.) increasingly want to concentrate their real estate allocations with fewer investment managers and those that can scale will be the winners.

Download the report.

Aaron Jodka

Aaron Jodka Nicole Larson

Nicole Larson