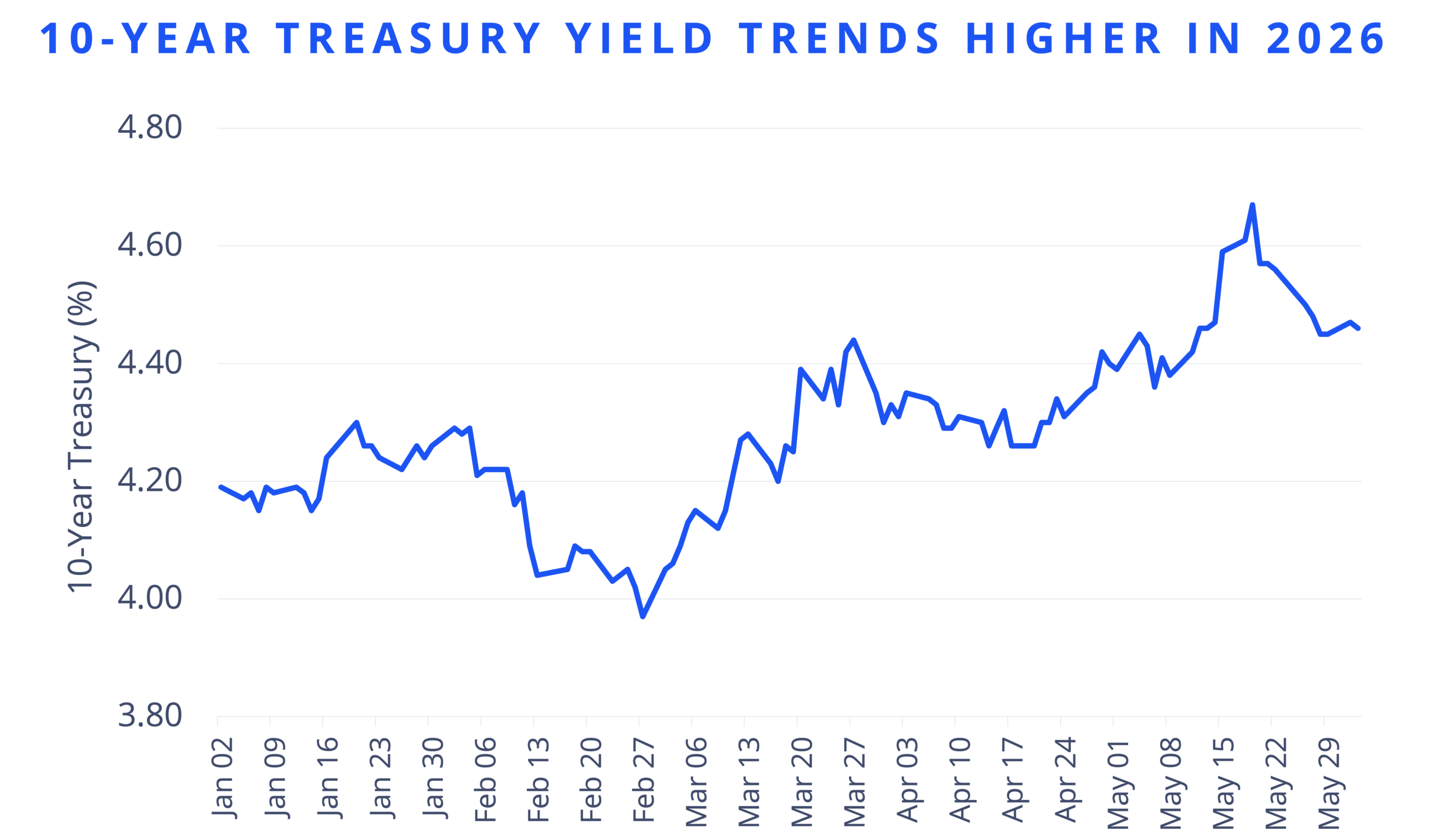

- Treasury yields have moved into a sustained higher range, with the 10-year hovering near 4.5% and the 30-year around 5%.

- Elevated rates are reinforcing a “higher-for-longer” backdrop and tightening financial conditions.

- Cap rates have reset but remain below long-term norms, indicating further upside risk.

- Transaction markets remain in price discovery, with valuations lagging capital markets repricing.

Treasury yields are stabilizing at levels that materially raise borrowing costs, shifting the discussion from short-term volatility to a sustained higher-rate environment. As financing becomes more expensive and less predictable, underwriting has tightened — particularly for refinancing-sensitive assets — while buyers are resetting return expectations and sellers remain anchored to prior pricing.

Cap rates have moved higher since 2022, but the adjustment appears incomplete. Transaction cap rates currently exceed modeled levels, and historical spreads to Treasuries suggest additional expansion is possible if yields hold. At the same time, rate volatility is widening bid-ask spreads by increasing financing uncertainty, which is slowing deal volume and delaying price alignment.

Steig Seaward

Steig Seaward

Cap rates may have further to run if Treasury yields remain elevated.

The result is continued downward pressure on valuations, driven by higher borrowing costs, potential cap rate expansion, and tighter leverage. With capital markets adjusting faster than property pricing, CRE remains in an ongoing repricing cycle that could extend if yields stay elevated.

Charles Dilks

Charles Dilks Victoria Abbasi

Victoria Abbasi Miles Rodnan

Miles Rodnan

Colliers Insights Team

Colliers Insights Team