Stephen Newbold

Stephen Newbold

The rapid escalation in sublease space has been a dominant feature of the U.S. office sector’s pandemic-driven downturn. There are now signs that the tide is slowly beginning to turn.

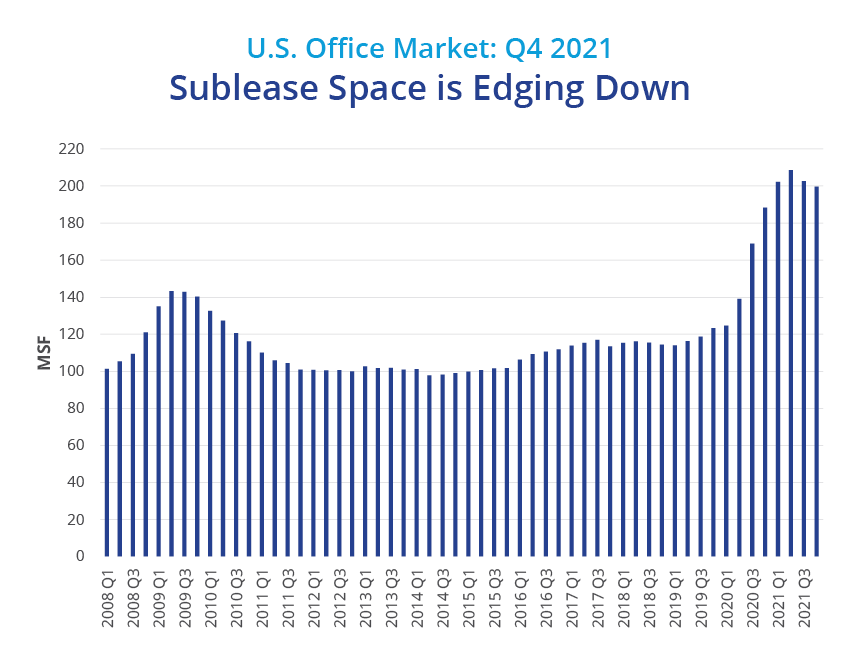

There is currently 199.7 million square feet of sublease space available across the U.S. office market, down from the record 208.8 million square feet posted in Q2 2021. While this remains significantly higher than the prior peak of 143.3 million square feet seen in mid-2009, Q4 2021 saw the amount of sublease space fall for the second successive quarter.

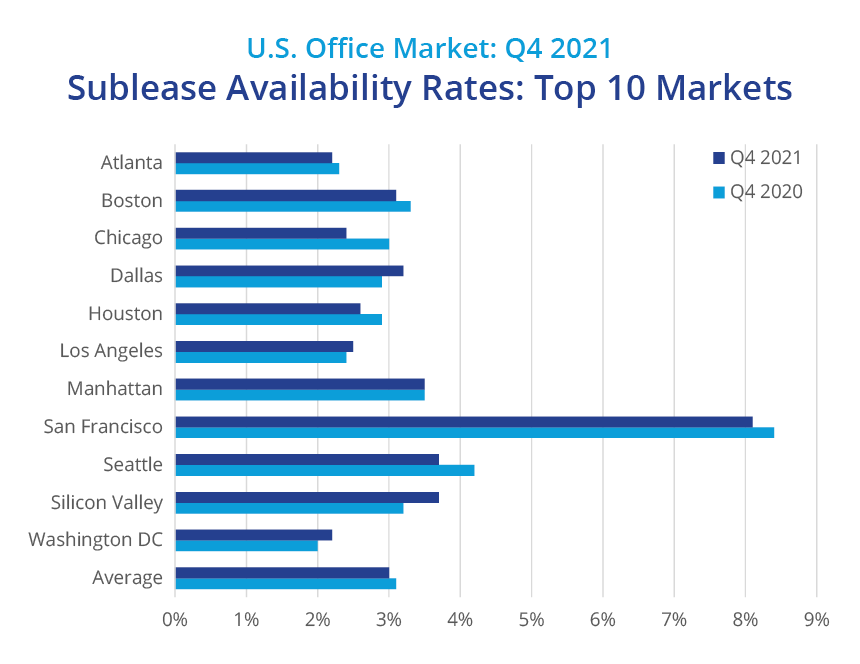

Significant variations persist in the impact of sublease space on the top 10 U.S. office markets. Total sublease space available across these markets stands at 89.8 million square feet, down from a peak of 100.5 million square feet in Q2 2021. Just over one-fifth of this space (18.6 million square feet) is in Manhattan. Dallas has the next highest amount, with 9.8 million square feet, followed by Washington, D.C. (9.7 million square feet) and San Francisco (7.9 million square feet).

Encouragingly, only three of these markets saw sublease space increase in the second half of 2021: Dallas, Silicon Valley and Washington D.C. Several markets saw a sizeable drop in their sublease total during this period, including Boston (down by 14.8%), Seattle (down by 12.6%) and Manhattan (down by 10.8%).

Square footage alone tells only part of the story. A more compelling statistic is the sublease availability rate. In this regard, San Francisco remains by far the most beleaguered market with an 8.1% sublease availability rate. A series of major givebacks by tech firms, some of whom have chosen not to occupy new premises that were pre-leased, has been a key factor in driving up these levels.

On a positive note, Sephora recently announced that it would be subleasing 16 floors totaling 286,000 square feet at the Salesforce Tower, which had been one of the most prominent sublease offerings in downtown San Francisco.

Two more tech-driven markets, Seattle and Silicon Valley, follow next, each with a 3.7% sublease availability rate. The average rate across the top 10 markets is 3%. Atlanta and Washington, D.C. are the least impacted, with both having a 2.2% sublease availability rate.

A good portion of the sublease space on the market is of Class A quality, with high-end fit-outs and decent remaining term. Such space is providing competition to the direct leasing market as it is being offered at a significant rental discount. In a period of uncertainty over future work patterns, business performance and occupancy needs, such space is an attractive option for firms waiting for clarity on the future.

The average discount in asking rents between Class A direct and sublease space in the downtown areas of the top 10 office markets has been trending in the 25% to 30% range, and currently stands at 25.8%. Given their CBD vacancy rates of over 25%, it is not surprising that Houston and Dallas have high sublease rental discounts at 50.6% and 34.7%, respectively. Downtown Chicago also ranks high with a 35.8% discount. Los Angeles and San Francisco have by far the lowest discounts, with both at under 10%.

What lies ahead? Once firms with active office requirements return to the market and leasing velocity picks up, landlords are expected to become more competitive. Asking rents for direct Class A space mostly held firm over the past year. However, the gap between asking and starting rents has widened due to increased concessions on offer.

Look for the volume of sublease space to trend down further in 2022 as more firms return to the office and decide to utilize previously offered space. Looking further ahead the office sector is in transition while users assess potential shifts in working practices, business location and space utilization. However, once occupancy needs are established and business confidence rises, we anticipate a pick-up in direct leasing activity, although sublease space should continue to weigh on the market in the short-to-medium term.

Anthony Shell

Anthony Shell

Andrew Steele

Andrew Steele

Aaron Jodka

Aaron Jodka Michelle Cleverdon

Michelle Cleverdon