Stephen Newbold

Stephen Newbold

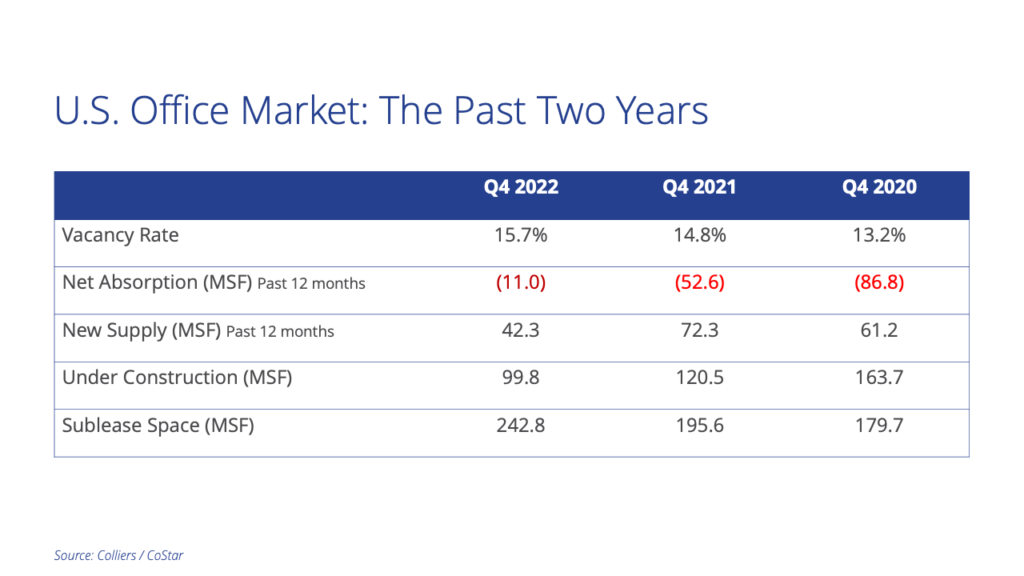

The U.S. office market closed out 2022 in downbeat fashion. Net absorption turned negative in Q4 2022, while vacancy rose, and sublease space hit a new record high.

The U.S. office vacancy rate stands at 15.7%, an increase of 30 basis points in the fourth quarter. Vacancy is still below the prior peak of 16.3%, seen at the height of the Global Financial Crisis, but will equal this level by mid-2023 if the current pace of vacancy increases is sustained.

et absorption, which measures the change in occupied office inventory, was positive in 43% of the metro office markets tracked in our national survey, down from 52% in the third quarter. National office absorption totaled negative 14.1 million square feet, more than offsetting the modest gains seen earlier in the year resulting in an annual net absorption total of negative 8.6 million square feet.

Reflecting this shift in fortunes, 12 metro markets posted negative absorption above 500,000 square feet. Occupancy losses in the fourth quarter were led by New York City (negative 4.3 million square feet), Greater Los Angeles (negative 1.8 million square feet) and Minneapolis (negative 1.5 million square feet). Conversely, positive absorption was led by Baltimore, Orlando, and Salt Lake City.

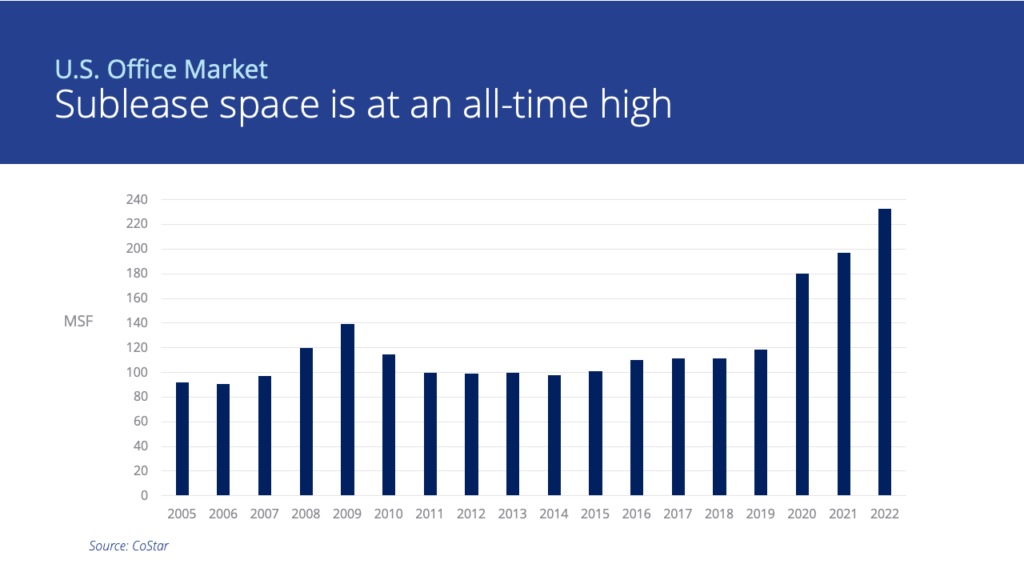

There is a record 242.7 million square feet of sublease space available across the U.S. office market, up from 232.8 million square feet in Q3 2022, and significantly higher than the prior cycle’s peak of 143.3 million square feet seen in Q2 2009. As firms continue to evaluate their post-COVID real estate needs, sublease space will remain a cost competitive, short-term option until there is greater clarity on business direction.

Construction activity continues to slow. Currently, 100.6 million square feet are underway, which is down 39% from this cycle’s peak of 164 million square feet in Q3 2020. The New York metro area has by far the largest amount of ongoing construction, at 15.3 million square feet, followed by the San Francisco Bay Area with 10.7 million square feet, which is mostly focused on Silicon Valley, and Seattle with 7.6 million square feet.

Asking rates are, by and large, showing little change. However, the gap between asking and effective rents remains significant due to generous concessions on offer. For example, tenant improvement allowances of $100 per square foot or more, plus 12 months of rent abatement, are available in several major markets when a tenant signs a new 10-year lease on Class A space.

There is considerable debate and speculation regarding the future of the U.S. office sector. The return to the office remains slow. Most tenants are adopting hybrid working with a minimum of three days in the office per week emerging as the common standard.

Is a market correction ahead? Firms continue to recast their property strategies focusing on how much space will be needed going forward and where it should be located. Evidence of tenant downsizing is increasing, with space reductions of at least 20% to 30% being implemented by large occupiers. Uncertainty in the economy continues to cloud the picture, further impacting the timing of such decisions. Existing lease commitments will also restrict the ability to implement change.

Pending a resurgence in demand, vacancy rates and sublease availability are set to continue to rise over the year ahead, placing increased pressure on rents. In addition, retrenchment in the tech sector, which has been a key driver of leasing volume, could compound this trend.

Where are the opportunities? Performance and demand differentials are expected to widen. This should be most evident between space class, but will also be seen between and within markets, and different business sectors. Quality will win out as firms seek the optimal work experience to retain and attract the best talent and bring employees back to the office. ESG initiatives offer owners an additional opportunity to differentiate their assets from the pack.

Anthony Shell

Anthony Shell

Andrew Steele

Andrew Steele

Aaron Jodka

Aaron Jodka Michelle Cleverdon

Michelle Cleverdon