U.S. National Research

U.S. National Research

Demand in the U.S. industrial sector has begun to moderate as economic headwinds, including persistent inflation, rising interest rates, and falling consumer confidence, linger. After a fruitful period of record-breaking industrial fundamentals, including occupancy gains, new development, lease rate increases and low vacancy, the industrial sector is beginning to show signs of softening. As a result, sublease space has significantly increased in recent months, with an elevated number of large spaces (greater than 200,000 square feet) added back to the market. The amount of available sublease space has risen nearly 46% since the start of the year and is expected to grow even higher in the coming months as occupiers evaluate their space needs.

Occupiers may have overestimated the amount of space needed to satisfy a just-in-case inventory strategy. Inventory control is beginning to backpedal to fewer days in the warehouse, which could impact industrial demand. As a result, the just-in-case strategy will remain an industrial driver, but companies will utilize less space than previously expected. The excess of space leased during the pandemic seems no longer necessary for some occupiers.

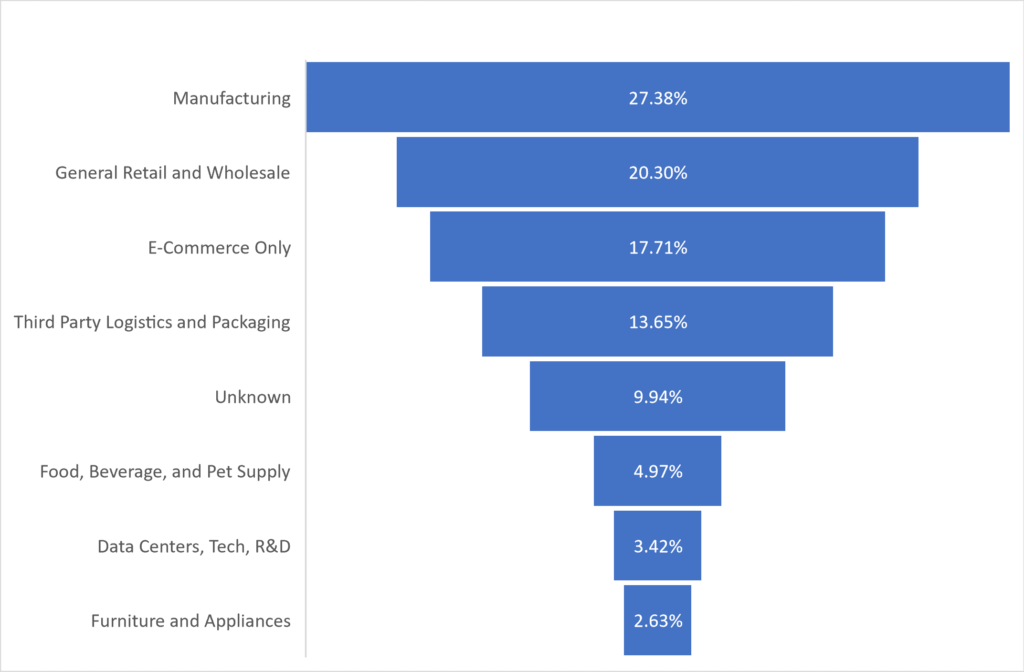

Interestingly, manufacturing companies have given back the most space over the last 12 months, accounting for 27.4% of newly available sublease space on the market. Retailers and e-commerce companies also added considerable space for sublease throughout the year. For example, The Coleman Co., a manufacturer of outdoor recreation products, has offered their massive 1.1-million-square-foot distribution center in the Kansas City market for sublease. The facility, built in 2009, was the Kansas City area’s first distribution center to top one million square feet.

Additionally, it is interesting to note that some of the available sublease space is listed in facilities still under construction, suggesting that space pre-leased prior to projects delivering is already being given back to the market. The areas with pre-leased space available for sublease include desirable core markets, including Atlanta, the Inland Empire, and northern New Jersey. With the full pipeline of projects yet to be delivered, overall vacancy will likely increase as new space and additional sublet space is added to the market in the coming year. However, it’s important to remember that although industrial demand is decelerating, occupancy gains remain well-above pre-pandemic levels. While it may seem like a sharp drop in demand, large occupiers including major retailers, 3PL companies, and food and beverage companies will continue to expand in 2023. Thus, the industrial downturn should be temporary, and the industrial sector will remain a desired asset for occupiers and investors alike.

Craig Hurvitz

Craig Hurvitz

Don Moss

Don Moss