Miles Rodnan

Miles Rodnan Andrew Wellman

Andrew Wellman Colliers Insights Team

Colliers Insights Team

- After the GFC, the District of Columbia posted low vacancies and steady demand.

- Negative absorption in 21 of the past 23 quarters has pushed vacancy above 20%.

- Conversions are starting to put a lid on the vacancy run-up and stand to support the market going forward.

- Project types vary across the wider metro area, with office-to-residential conversions popular in the District. At the same time, close-in markets and outer suburbs regularly see teardowns and rebuilds into multifamily or townhomes.

- Washington, D.C., has long been a top choice for office investors. Future changes to fundamentals make it a compelling value play today.

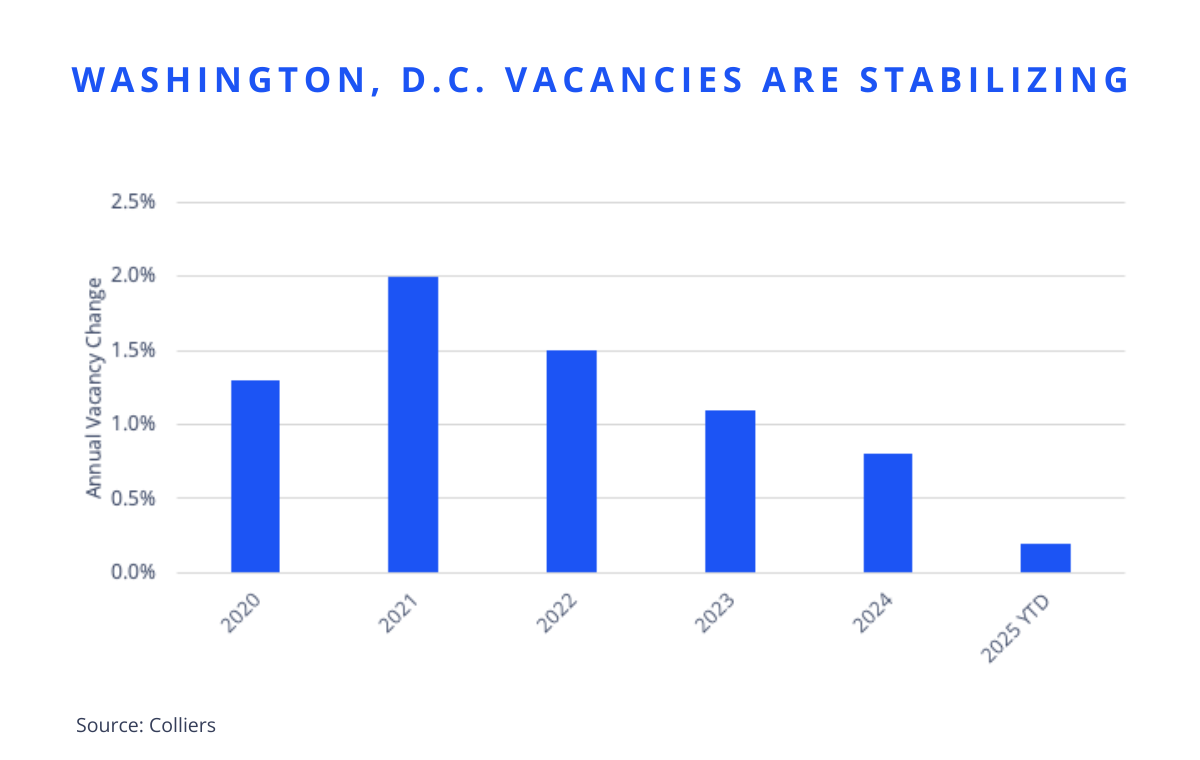

From 2009 to 2019, the overall vacancy rate in the District of Columbia hovered between 10% and 13%. Coming into 2020, the vacancy rate was 13.6%. With the shift in office work dynamics and a continued contraction of federally leased space, it reached a peak of 20.6% in the second quarter of this year, a result of occupancy losses in 21 of the past 23 quarters. However, vacancy increases have started to slow. Space is still being returned to the market, but vacancies have risen by only one percentage point since the start of 2024. Even with the delivery of space in early 2024, more than 1.5 million square feet of inventory has been removed from our tracked set, with a large majority being conversions.

Prior to the pandemic, conversions leaned toward office-to-residential or hospitality in the District and toward lab in the Maryland suburbs. However, the biotech sector has cooled from its peak, and conversions are now focused on residential projects or limited demolition and construction of new trophy offices. One of the largest and most recent examples to break ground is Henderson Park and Lowe’s Portals project. The former office building at 1250 Maryland Avenue SW, which had long housed government contractors and federal tenants, will now be home to 428 units. Another notable conversion in the heart of downtown D.C. is 1201 Connecticut Avenue, a 190,000 SF office building currently being converted into a 161-unit residential building.

“With inventory shrinking, office investment in and around the nation’s capital should garner increased investor attention.”

Additionally, in the surrounding suburbs, Northern Virginia has seen an influx of office-to-residential conversions in the Alexandria and Arlington County areas. In contrast, Maryland has seen conversions shift from life sciences to residential. In Montgomery County, MD, and the outer suburbs of Northern Virginia, a different type of redevelopment play is emerging, with office buildings being demolished to make way for townhome development.

While Class A and trophy assets across the region remain leasable, aging lower-class buildings will likely continue to be evaluated for conversion or demolition. Although many conversions are rumored, it is anticipated that more than 10 million SF could be removed from inventory across the metro area. However, given the cost of conversion and an evolving economic backdrop, it is uncertain how many of these projects will come to fruition.

Steig Seaward

Steig Seaward

Marianne Skorupski

Marianne Skorupski