Komail Khaja

Komail Khaja Samantha Wassum

Samantha Wassum

Richmond’s definition of trophy office space is evolving. Once associated almost exclusively with downtown high-rises, the desire for premier office product is increasingly emerging along suburban corridors in Henrico County and in Richmond City, outside of the CBD. Submarkets such as Glenside/I-64 and Midtown/Scott’s Addition areas are seeing a wave in both new construction and the repositioning of legacy assets into high-end workplaces. This shift reflects a growing tenant preference for top-tier finishes and amenities paired with suburban accessibility, even as some projects move forward with limited preleasing, underscoring developer confidence in long-term demand outside the CBD.

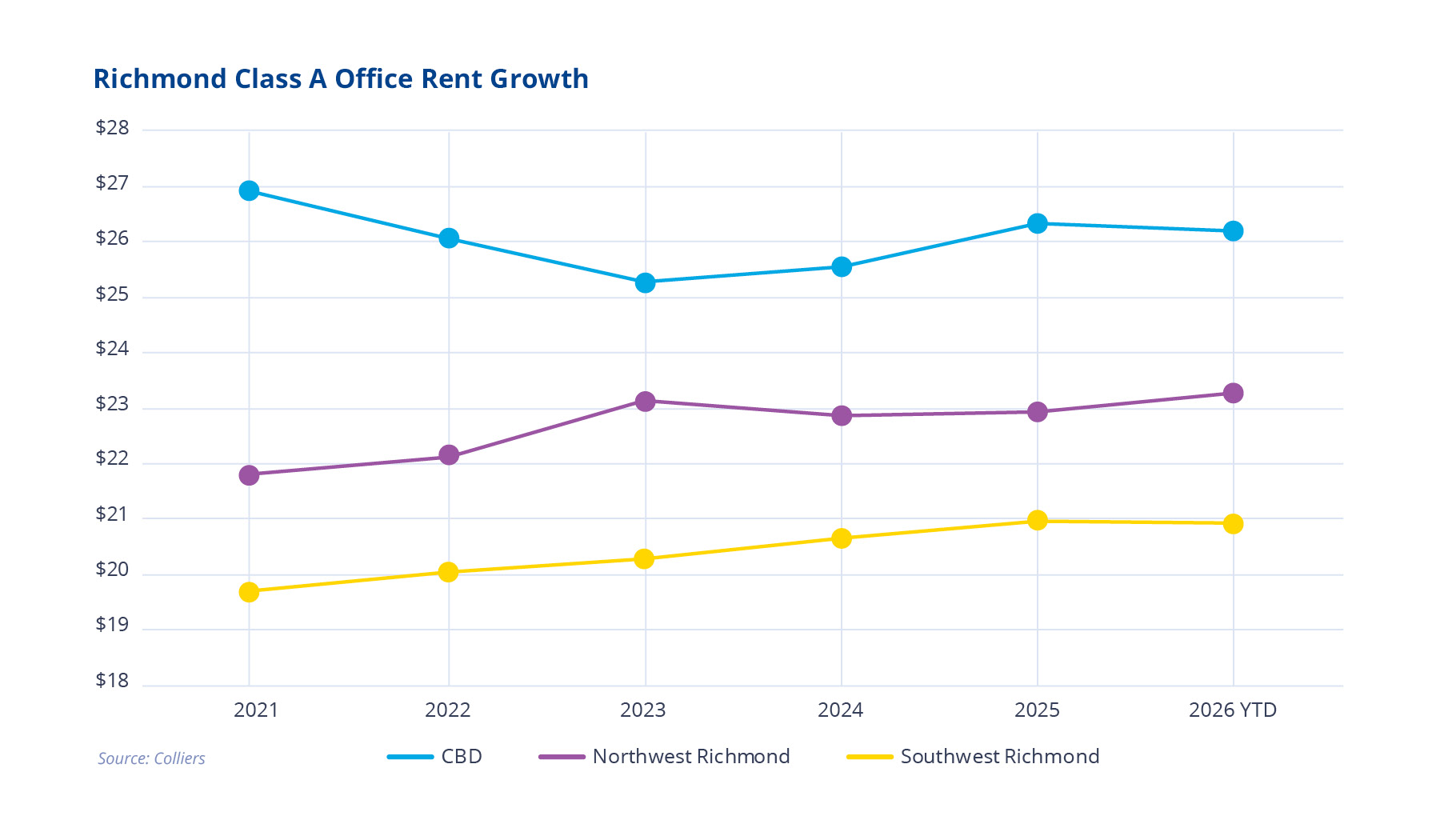

This evolving geographic focus is already being reflected in rent performance across the market. Class A office rent growth has increasingly favored suburban submarkets over the urban core in recent years. While CBD rents have remained effectively flat, declining approximately 3% between 2021 and 2026 despite recent stabilization, both the Southwest Quadrant (Chesterfield County) and the Northwest Quadrant (Henrico County) have demonstrated consistent upward momentum. The Southwest Quadrant recorded cumulative rent growth of roughly 6% over the five years, while the Northwest Quadrant outperformed with approximately 7% growth, driven by stronger early-cycle increases. This divergence reinforces a broader rebalancing of demand, as newer suburban products and ease of access continue to support stronger pricing power relative to the CBD.

Supporting this trend is a growing pipeline of new development and repositioned assets that are redefining what constitutes “trophy” space in the Richmond market. Projects such as Midtown 64 (6604 W Broad Street) and the Diamond District mixed-use development (2727 Diamond View Drive) exemplify this shift, introducing modern, amenitized office environments into suburban and emerging mixed-use areas. Notably, both developments are reportedly commanding rents north of the mid-$40s per square foot, further demonstrating tenant willingness to pay a premium for high-quality space that aligns with evolving workplace expectations.

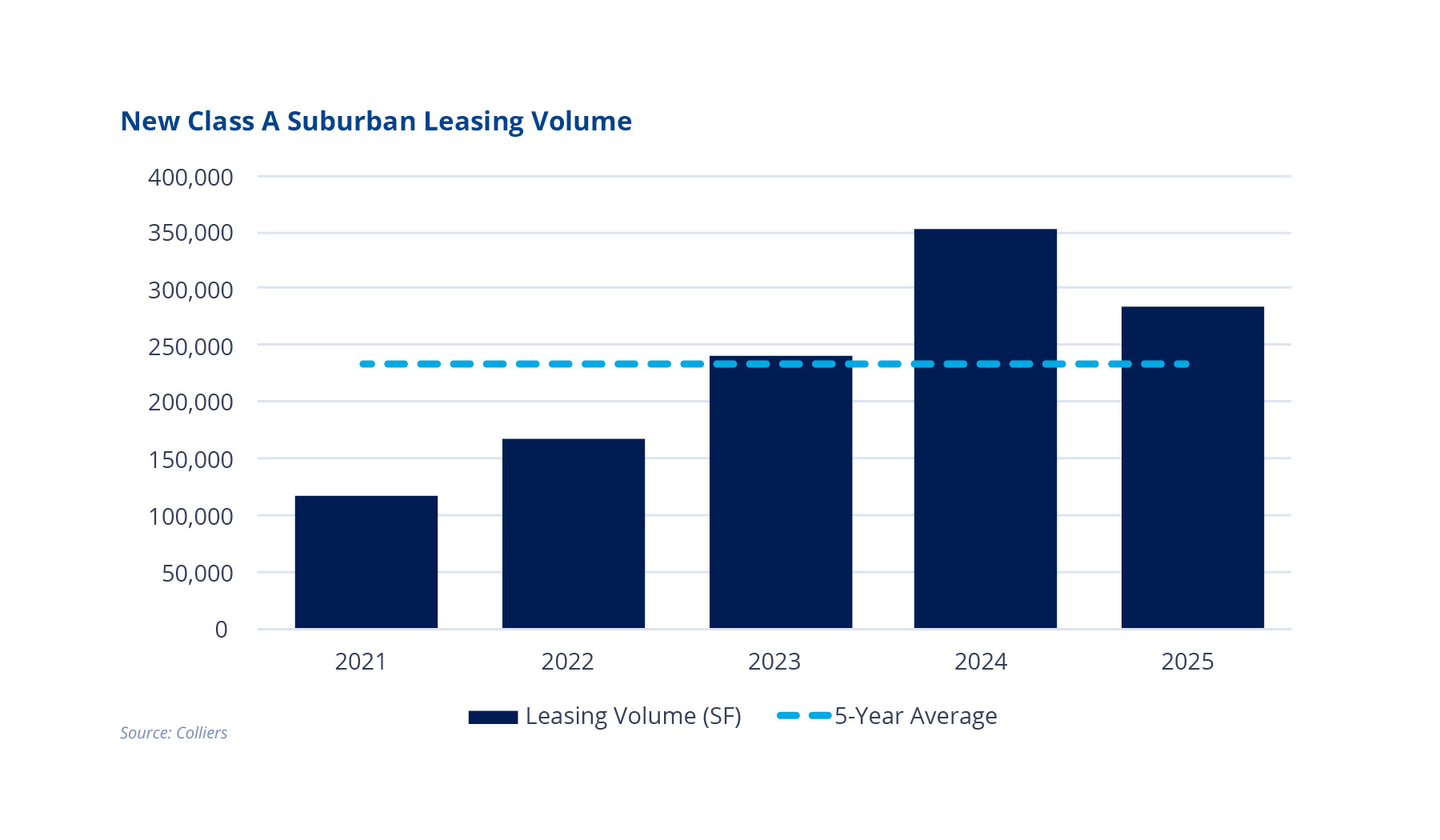

Leasing fundamentals further validate this structural shift in demand. The data reflects a clear upward trajectory in new Class A suburban office leasing activity over the past several years, reinforcing a broader recovery narrative despite some near-term variability. Leasing volume increased 43% from 2021 to 2022, followed by another 43% gain in 2023. Momentum accelerated further in 2024, with activity reaching a peak of nearly 353,000 square feet, representing a 46% annual increase and a nearly threefold expansion from 2021 levels. While 2025 shows a modest pullback, it remained above the five-year average. Taken together, this pattern suggests that leasing demand is structurally trending upward, with three consecutive years of outsized growth followed by a measured correction that appears more indicative of normalization after peak activity rather than a fundamental shift in demand. The first quarter of 2026 recorded just over 87,000 square feet of leasing activity, reinforcing the presence of sustained tenant demand and suggesting continued stability as the year progresses.

Viewed collectively, these trends point to a market in transition. As tenant preferences continue to prioritize quality, accessibility, and amenitization, Richmond’s trophy office landscape is expanding beyond its traditional urban core. While near-term fluctuations in leasing activity are to be expected, the underlying fundamentals, including rent growth in suburban submarkets, premium pricing on new product, and sustained leasing momentum, indicate that demand for high-quality office space remains intact. The result is a more diversified and geographically balanced trophy segment, positioned to evolve alongside changing workplace strategies and occupier needs.

Marianne Skorupski

Marianne Skorupski

Brennan Yerman

Brennan Yerman Franklin Wallach

Franklin Wallach

Ed Lawrence

Ed Lawrence