Nicole Larson

Nicole Larson Mike Otillio

Mike Otillio Baily Datres

Baily Datres Patsy Fretwell

Patsy Fretwell

For the First Time in History, All Top Retail Construction Markets Are in One State

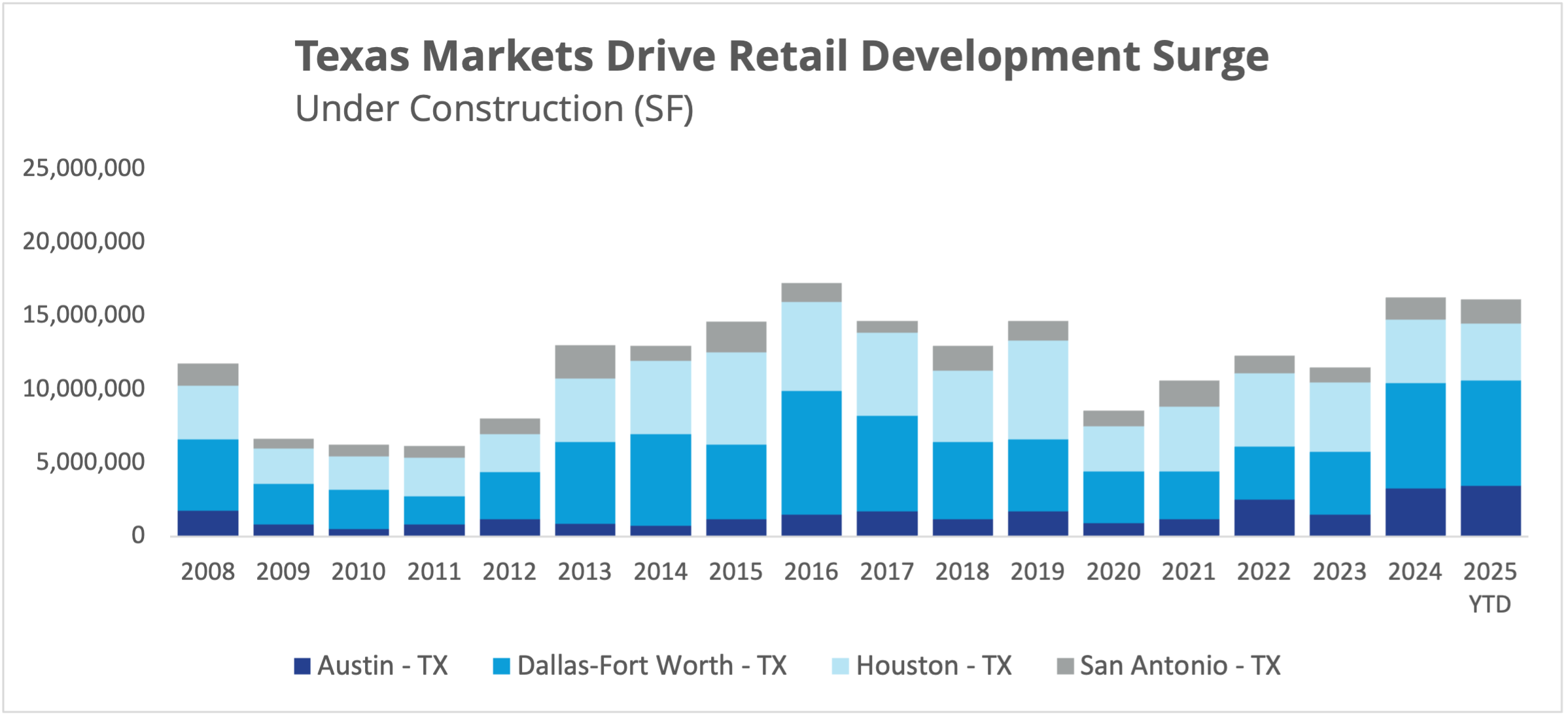

For the first time in history, Texas is leading the nation in retail construction, fueled by its booming population and strong in-bound migration. Between January 2021 and January 2025, the state recorded a positive net domestic migration of 0.9%, and post-pandemic, 19.1% of Californians who relocated chose Texas — a clear sign of its appeal for affordability, job opportunities, and a pro-growth environment. Over the past decade, retail development has kept pace with this influx, with developers delivering an average of 6 to 7 million square feet of new retail space per quarter from 2016 to 2019, holding vacancies near 4% while meeting demand from national chains and local operators. Although construction slowed in 2020 amid pandemic-driven uncertainty, activity quickly rebounded, and by early 2025, more than 17 million square feet was under construction — one of the highest levels in the country.

This starkly contrasts with the national landscape, where construction activity remains historically low. Just 6 million square feet of retail space was delivered nationwide in the second quarter of 2025, bringing total space under construction to 47.9 million square feet. Elevated financing and construction costs continue to limit new standalone retail development, while demand for multifamily, industrial, and mixed-use projects drives developer focus elsewhere. Since 2020, only 21 million square feet of newly built retail has been listed for lease nationally, less than 5% of all available space. Notably, nearly one-third of that first-generation space is concentrated in Texas, underscoring the state’s position at the center of the nation’s retail development pipeline.

Austin

Austin’s retail construction acceleration tells the story of a market that spent over a decade being artificially constrained by its success. Austin currently leads in overall construction intensity with 2.8% of inventory under construction, compared to 1.5% in Dallas-Fort Worth, which leads in total inventory growth. The city’s transformation from a quirky college town to a central tech hub happened faster than its retail infrastructure could adapt, creating the kind of supply-demand imbalance that developers dream about but rarely encounter in mature markets. The current construction surge represents a long-overdue correction to years of underdevelopment, as the market finally builds the retail infrastructure necessary to support its evolved economic identity. Austin’s situation exemplifies how Texas markets have been quietly accumulating pent-up demand while other regions struggled with oversupply.

Austin saw minimal retail development for over a decade, contributing to extremely tight market conditions. The market achieved the highest occupancy among Texas metros at 97.1% in 2024 Q4, demonstrating the “underbuilt” nature of Austin’s retail inventory. Limited construction through the 2010s created today’s demand imbalance, with consistent net absorption averaging over 2 million square feet annually. The market’s fast-growing population at a rate of 2.6%, rising household incomes, and robust consumption continue to garner attention from retailers, with much of this growth occurring in suburban regions that drive retail demand. An uptick in newly constructed space availability could help meet future demand, with substantial square footage projected for delivery, keeping Austin a national leader for inventory growth. However, the high percentage of space under construction that is already pre-leased or owner-occupied suggests a minimal impact on vacancy rate outlooks, demonstrating Austin’s ability to maintain exceptional occupancy levels even during its most aggressive construction period and confirming that Texas markets have achieved economic maturity to sustain intensive retail development.

Dallas-Fort Worth

The Dallas-Fort Worth metroplex exemplifies the new Texas retail paradigm, where decades of conservative development philosophy have suddenly given way to unprecedented construction activity. DFW leads the nation in retail space under construction with 7.2 million square feet in the pipeline as of Q3 2025. DFW’s construction boom is driven by its massive economic scale: 296,828 businesses, 3.36 million employees, and 8.34 million residents. Historically, Texas markets were built cautiously, scarred by the overbuilding cycles that plagued other regions during economic downturns. DFW’s current construction surge represents a fundamental shift in developer confidence, driven by the metro’s transformation into a true economic powerhouse that rivals coastal markets in scale and sophistication. The region’s retail expansion reflects something more profound than mere population growth—it signals the maturation of Texas as a business destination that can sustain the dense, high-velocity retail environments previously associated with established East and West Coast markets.

As the market approaches the second half of the year, Dallas-Fort Worth finds itself navigating a complex landscape where it maintains its position as the leader for tenant demand with a robust net absorption averaging around 3.6 million square feet annually, even as headline-making store closures have created the first instance of negative net absorption in over two years. The construction pipeline remains robust, with new inventory providing retailers the space needed to enter and expand without drastically impacting vacancies, particularly in northern Collin County, where population growth has been strongest. DFW’s construction boom is particularly significant because it represents the convergence of Sun Belt demographics with traditional retail market dynamics, creating the kind of concentrated economic activity that supports premium retail development. Strong annual rent growth of 4.1%, outpacing the other Texas metros, has made new groundbreakings economically viable. At the same time, the market’s continued leadership in domestic inbound migration provides ongoing support for retail demand even as total population growth has moderated.

Houston

Houston’s retail sector continues to expand with the metro’s surging population, thriving housing pipeline, and diversified economy. Now home to more than 7.6 million residents — and ranking second nationally in numeric population growth for two consecutive years – the region is fueling demand across the retail spectrum, from daily essentials to experiential destinations featuring entertainment venues. Residential growth remains a key driver, with 11,000 building permits issued in the first two months of 2025 — more than any other U.S. market — and Houston leading the country in top-selling master-planned communities. Growth is robust in fast-growing suburban areas, where retail is being added to support everyday needs and elevate the quality of life.

Retail market fundamentals remain healthy, with vacancy rates within the historical 5%-6% range, supported by consistent leasing activity, stable rents, and a development pipeline totaling 3.6 million square feet. The market continues to absorb new supply while adapting to shifting consumer behavior and evolving tenant strategies. Houston’s recent emergence in the Michelin Guide marks a milestone for the city’s culinary scene, reflecting its cultural evolution and expanding restaurant diversity. The grocery sector remains a cornerstone of retail demand, led by H-E-B, which now commands over one-third of the market, and continues to spur surrounding development with each new store. In addition, Sprouts is actively backfilling space, while Walmart and Target roll out next-generation prototypes. With competitive land and construction costs, resilient tenant demand, and an evolving mix of uses and experiences, Houston remains one of the nation’s most dynamic and attractive retail markets.

San Antonio

San Antonio’s emergence as a significant retail construction market represents the most compelling evidence of Texas’s statewide retail transformation. Historically positioned as the most conservative and stable of the major Texas metros, San Antonio has maintained high retail occupancy, averaging over 96% for consecutive years through cautious development and historically modest construction pipelines. The city’s recent retail expansion reflects a broader economic awakening, as decades of gradual business development and population growth have finally reached the threshold where significant retail investment becomes not just viable but essential. San Antonio’s story demonstrates how Texas’s retail construction dominance extends beyond the obvious high-growth markets to encompass the entire state’s economic ecosystem.

As one of the nation’s most popular destinations for domestic migration, the San Antonio retail market continues to experience significant demographic momentum, adding substantial new residents over recent years, attracting their purchasing power, and creating tailwinds for retail real estate. In 2025, San Antonio has increased retail construction activity with 1.7 million square feet under construction, representing the most active construction period in recent years. Current occupancy remains tight at 96.3%. The market continues to demonstrate strong fundamentals with most new space pre-leased, preserving historically high occupancy levels. San Antonio also remains one of America’s fastest-growing large cities, bolstering retailer confidence. Despite positive demand formation, overall construction intensity remains lower than the rest of Texas’s major metros at 1.1% of its retail inventory due to historically conservative building activity and low financing availability. The market has largely assumed a relatively flat outlook for demand as otherwise optimistic local demographic tailwinds meet increasing macroeconomic pressures. Yet, local investors report encouragement from the tight market for space and the area’s growing consumer base. The historical context reveals how San Antonio’s development, along with Dallas-Fort Worth as the business hub and Austin as the innovation center is converging into a unified Texas economic region where retail demand is driven by complementary strengths rather than competing advantages — a convergence that, combined with the state’s unique ability to accommodate large-scale development, has created the conditions for Texas’s historic domination of national retail construction rankings.

Anjee Solanki

Anjee Solanki