Franklin Wallach

Franklin Wallach

- In 2025, Manhattan office leasing volume reached a six-year high, marking a watershed moment in the market’s post-pandemic recovery.

- Availability tightened, falling to its lowest point since November 2020.

- Sublet inventory also declined, reaching its lowest level since late 2019.

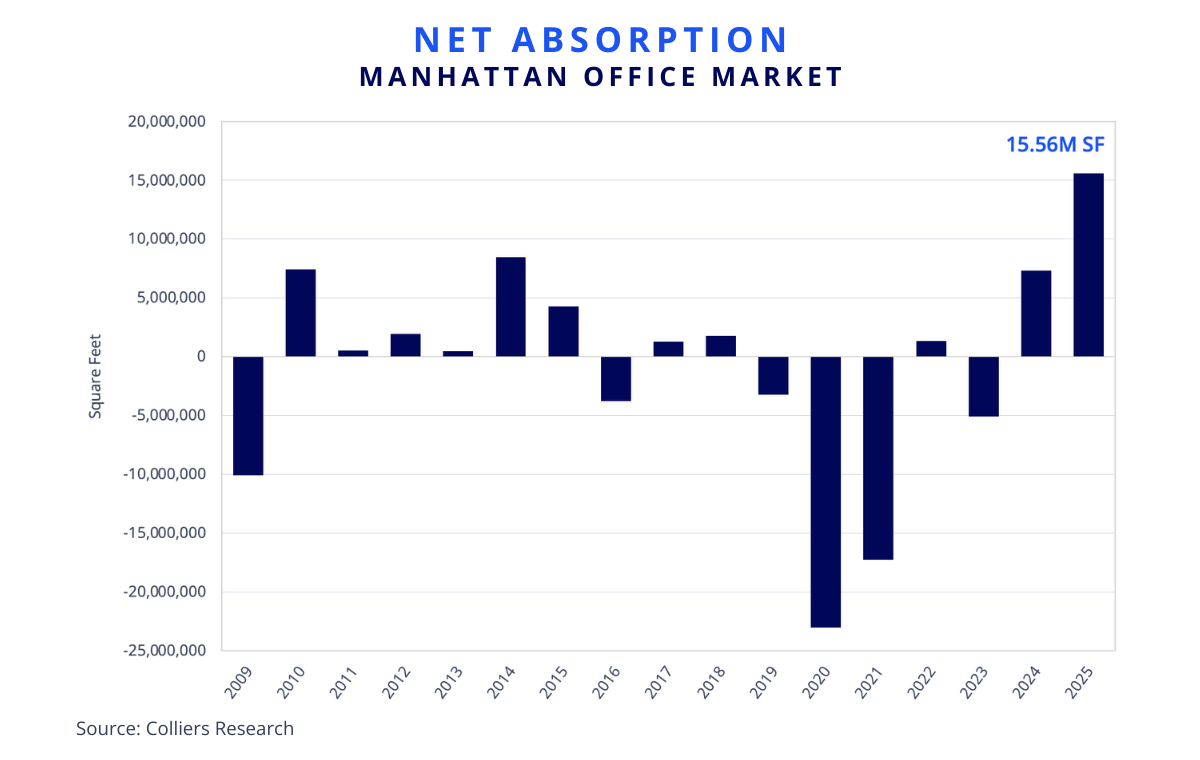

- Positive absorption totaled a record 15.56 MSF for the year, far surpassing the previous high of 8.44 MSF more than a decade ago. [1]

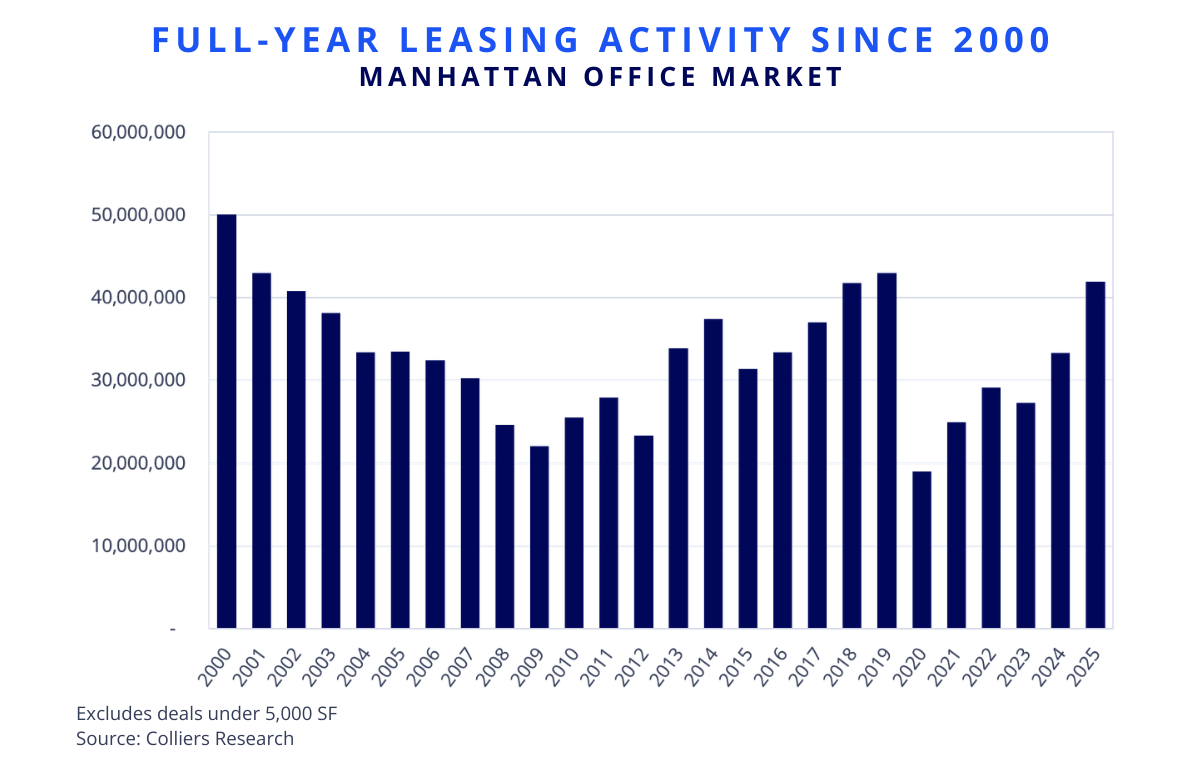

In 2025, several factors drove more than 15 MSF of positive absorption in Manhattan. Leasing demand totaled 33.34 MSF in 2024, comparable to typical yearly activity since 2000, before surging to 41.92 MSF in 2025. The uptick was fueled by flight-to-quality opportunities, return-to-office mandates, the reemergence of Manhattan’s tech sector, and strong demand from financial and professional services tenants. Mega-leases amplified this activity, including NYU at 770 Broadway (1.08 MSF), Jane Street Group at 250 Vesey Street (984,000 SF), and Deloitte at 70 Hudson Yards (807,000 SF). As a result, 2025 marked Manhattan’s highest yearly leasing total since 2019, just 2.4% below the pre-pandemic total that year.

Strong absorption in 2025 was buoyed by Manhattan’s rapidly tightening availability. Available supply grew nearly 37% since March 2020, reaching 73.61 MSF in December 2025. That figure was substantially lower than the post-pandemic peak of 98.05 MSF in February 2024 and the lowest level since November 2020. An increase in tenant activity and demand for high-quality, built, and furnished sublet space contributed to the dwindling available supply. Blocks of existing sublet space were also withdrawn due to reoccupancy by sublessors. Sublet inventory declined by 37% over the last 12 months to 11.41 MSF, the lowest level since October 2019.

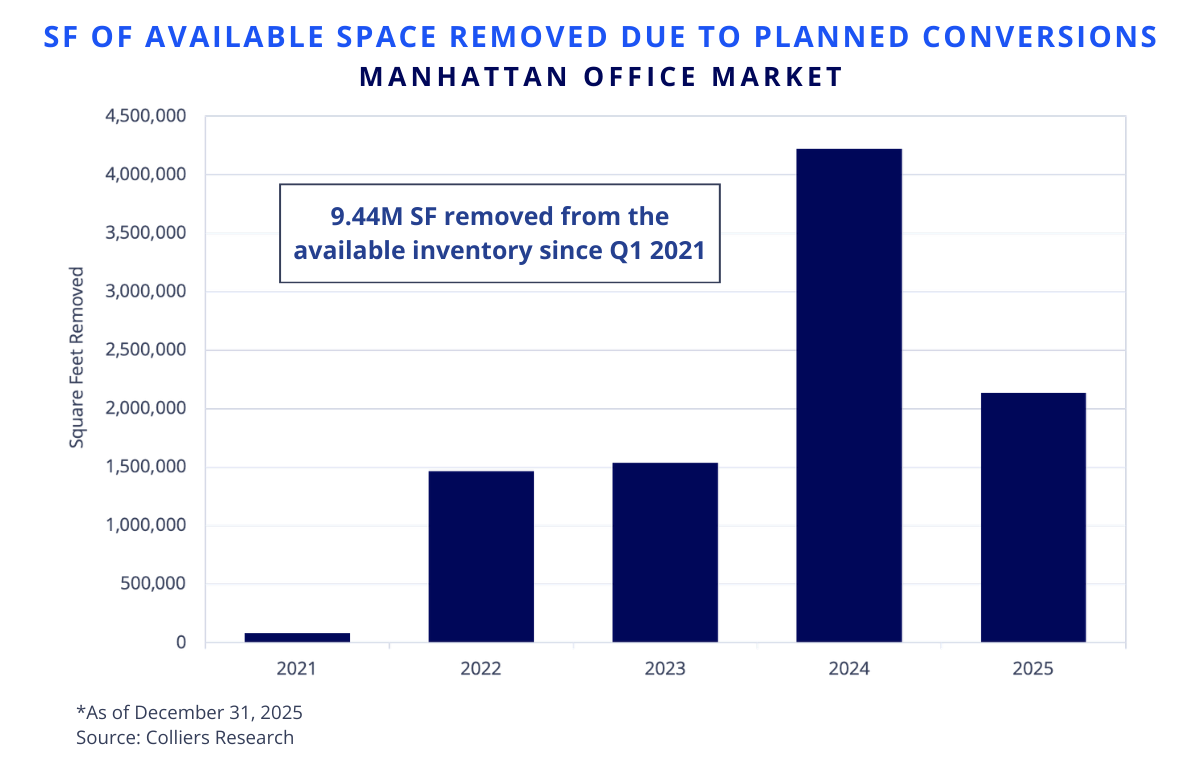

Supply was also reduced by the volume of space removed from the market for conversion to residential, hotel, storage, or other non-office use. Planned conversions totaled 2.14 MSF across 16 office buildings taken off the market in 2025. These removals not only reduced supply but also triggered a secondary wave of absorption as tenants in these buildings leased space and relocated within the market.

Manhattan’s record 15.56 MSF of positive absorption in 2025 was a clear indicator of the post-pandemic recovery in one of the world’s most consequential office markets. The key question for 2026 is whether the market will see another record level of positive absorption. The short answer is that it is possible, though unlikely. Net absorption in 2025 was nearly double the prior high of 8.44 MSF in 2014, making a repeat of that performance challenging given that much of the post-pandemic supply has already been absorbed.

Notes

[1] Record absorption in Manhattan’s office market reflects strong leasing demand and the gradual absorption of pandemic-era supply.

Steig Seaward

Steig Seaward