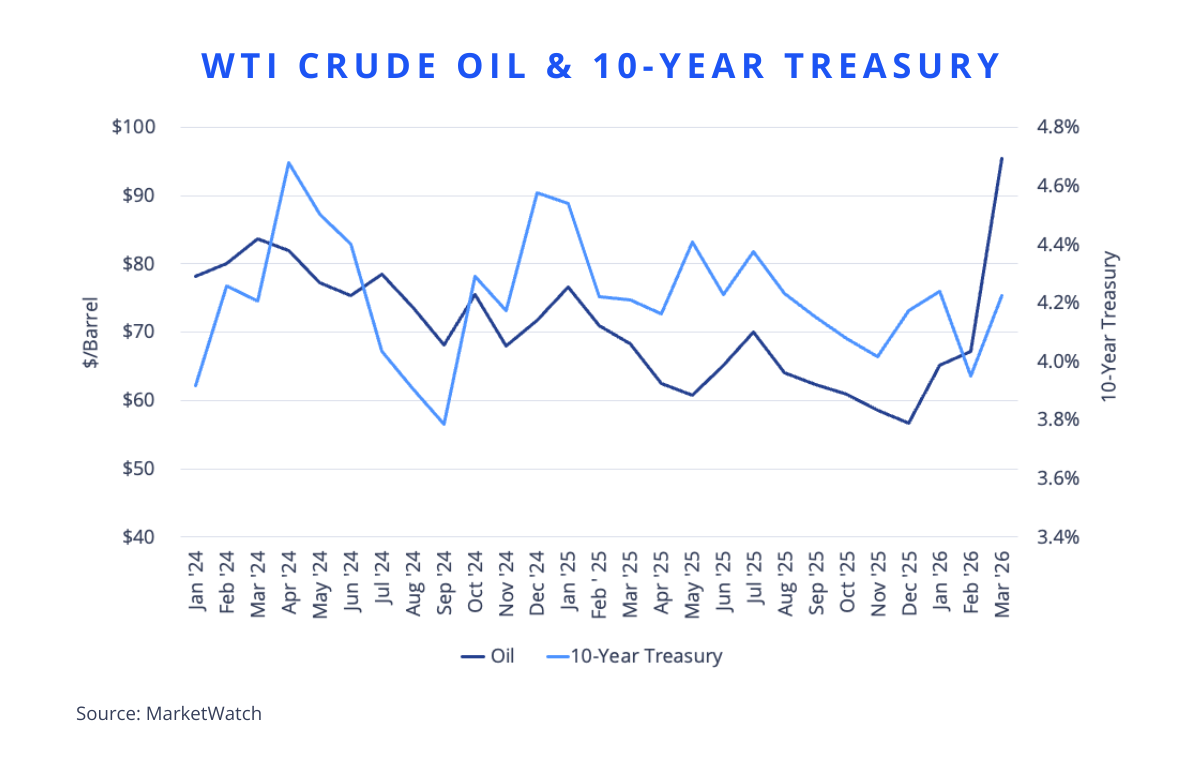

- Oil prices have surged following disruptions tied to the Strait of Hormuz, driving energy costs materially higher.

- Rising energy prices are lifting near-term inflation expectations, complicating the Federal Reserve’s policy calculus.

- The Fed is likely to remain cautious, reinforcing a data-dependent, wait-and-see stance.

- Treasury yields have been volatile but remain range-bound, with the 10 year constrained by competing inflation and growth signals.

Escalating U.S. and Israeli military action involving Iran has injected a fresh wave of volatility into global markets, with the most immediate impact seen in a sharp surge in oil prices. Oil markets have reacted forcefully, with crude prices jumping more than 35% in a single week and moving above $90 per barrel—one of the most extreme short-term rallies in decades. The rapid rise in energy costs is triggering a familiar chain reaction through global markets: higher oil prices quickly feed into transportation, utilities, and production inputs, pushing near-term inflation expectations higher and raising questions about monetary policy and long-term interest rates, even as longer-term inflation expectations remain relatively anchored.

This places the Federal Reserve in a familiar position. History shows that geopolitically driven energy shocks often complicate policy without fundamentally altering the longer-term outlook. During the 1973–74 oil shock, triggered by the Arab oil embargo following the Yom Kippur War, oil prices nearly quadrupled, inflation surged, and interest rate volatility grew entrenched as expectations became unanchored.

More recent episodes point to more restrained outcomes when shocks are shorter-lived. The 1990 Gulf War oil shock saw oil prices roughly double in a matter of weeks, lifting inflation expectations and Treasury yields initially before stabilizing as supply fears eased and the conflict concluded. Similarly, during the 2007–08 oil price surge, policymakers acknowledged the inflationary impulse from energy costs but emphasized credibility and anchored expectations, with long-term yields reflecting tension between inflation risks and weakening growth rather than a lasting reset.

Today’s environment is more similar to these later episodes. Oxford Economics’ base case still calls for rate cuts in June and September, but the war is increasing the odds against them. Higher energy prices are lifting near-term inflation risks and reinforcing the Fed’s cautious, data-dependent stance, leaving policymakers less inclined to signal confidence around near-term easing. As a result, market conviction around the timing of cuts has weakened, even if officials ultimately view the oil-driven inflation impulse as transitory.

Steig Seaward

Steig Seaward

Energy-driven inflation pressures are reinforcing the Fed’s cautious approach to rate cuts.

That tension is most evident in the 10-year Treasury. Surging oil prices raise the risk that inflation remains sticky, pushing term premiums higher and limiting the downside for long-term yields. Beyond oil, factors including political uncertainty, concerns over Fed independence, persistent inflation pressures, and elevated Treasury issuance are keeping term premiums firm, reinforcing a structurally higher floor for the 10-year. The result is a market caught between inflation risk and growth uncertainty, keeping the 10-year anchored within the narrow range that has held since last fall, despite sharp intramonth volatility. Until energy prices retreat or inflation expectations convincingly cool, long-term yields are likely to remain elevated.