- Credit spreads and lender risk pricing, rather than policy rates, are increasingly driving transaction activity.

- Despite Treasury yields remaining range-bound, credit spreads have widened and become more volatile.

- Lenders are embedding greater uncertainty into risk premiums, tightening proceeds, and shaping deal structures.

- At the same time, leverage availability has improved modestly but remains selective and uneven across lender types.

Despite elevated Treasury yields, rates have traded within a relatively narrow range in recent months. In a typical cycle, that stability would support improving transaction activity. Instead, Trepp data show that CRE credit spreads have widened across major property types, pushing all in borrowing costs higher even when base rates hold steady.

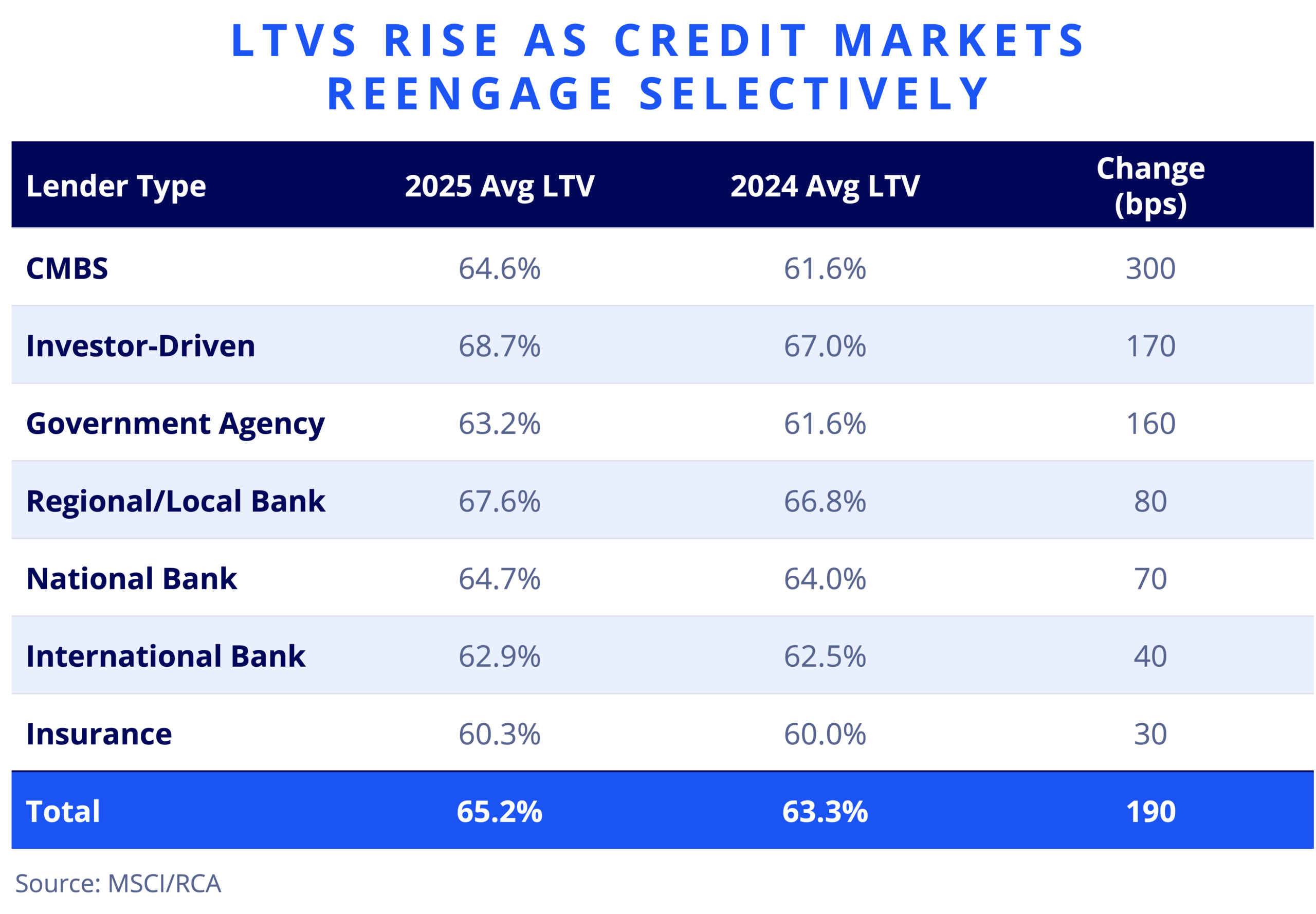

Lenders continue to emphasize downside protection amid uncertainty around asset fundamentals and refinancing risk. RCA data show that average loan-to-value ratios rose modestly in 2025, signaling a selective reopening of credit markets rather than a broad easing of conditions. Higher leverage remains concentrated among investor driven lenders, while banks and insurance companies have only marginally loosened underwriting standards.

Importantly, modestly higher LTVs have not offset wider credit spreads, meaning all in borrowing costs and debt service constraints continue to limit proceeds despite incremental improvements in leverage.

As a result, spreads, not Treasury rates, are increasingly determining leverage. Even modest spread widening can materially reduce loan proceeds, forcing buyers to add equity or reprice bids. In many cases, transactions are stalling not due to disagreement over long term value, but because current debt economics no longer support legacy pricing.

Steig Seaward

Steig Seaward

Even modest spread widening is reducing proceeds and forcing buyers to reprice.

Taken together, these conditions suggest that the next phase of market recovery will depend less on the timing of rate cuts and more on lenders regaining confidence that risk is adequately priced. Until spreads stabilize, credit pricing, not monetary policy, will remain the primary constraint on CRE deal activity.