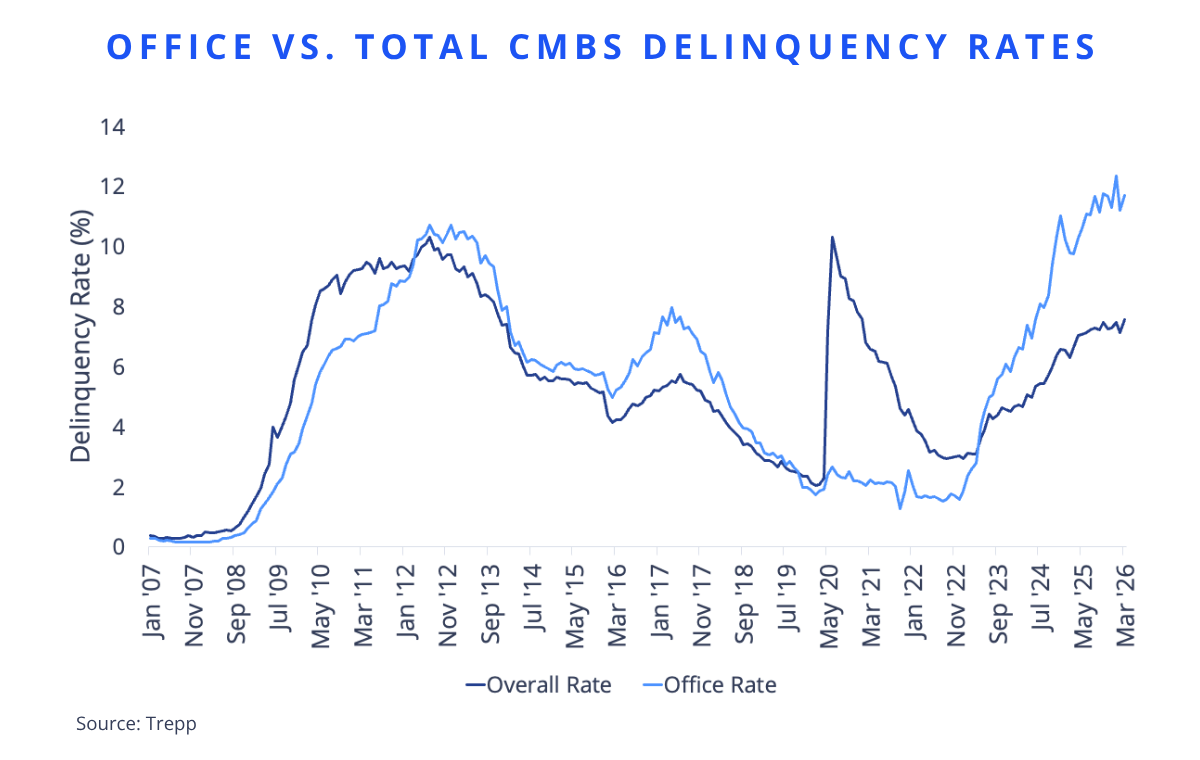

- Office CMBS delinquency registered 11.71% in March 2026, remaining near record levels despite a pullback from January’s peak.

- The prior cycle high of roughly 10.7% occurred in late 2012, several years after the Great Financial Crisis (GFC), underscoring how today’s stress exceeds past peaks.

- Current distress is being driven primarily by refinancing pressure rather than widespread operating failure.

- Delinquency volatility is amplified by concentration, with a small number of large office loans capable of moving headline rates month to month.

Office remains the primary source of stress within the CMBS market, even as delinquency rates eased modestly from recent highs. According to Trepp, the office CMBS delinquency rate stood at 11.71% in March 2026, down from the 12.34% peak reached in January, but still well above prior cycle highs and firmly within an elevated range that has persisted over the past year.

Historically, CMBS delinquency cycles have lagged broader economic downturns. Following the GFC, office delinquencies built gradually and did not peak until 2011–2012, as loans matured into tighter credit conditions and impaired valuations. That delayed peak reflects the long‑dated nature of securitized debt and the time required for refinancing stress to surface.

While the current cycle shares that maturity‑driven dynamic, it is unfolding more rapidly. Trepp characterizes today’s office stress as structural rather than cyclical, citing the combined effects of higher interest rates, weaker leasing demand, and lasting shifts in office utilization. Although office delinquencies declined modestly in March, Trepp notes that the sector remains in a high‑delinquency regime, with much of the stress tied to loans unable to refinance at prevailing rates.

Steig Seaward

Steig Seaward

Structural shifts in the office sector are compounding refinancing challenges.

Taken together, the comparison highlights a key distinction from the post‑GFC experience: prior office CMBS distress accumulated slowly over time, while the current cycle reflects faster adjustment and sustained pressure, driven by refinancing friction and structural demand headwinds.