- Loan extensions have postponed pricing resolution but have not solved refinancing challenges.

- Higher interest rates have diminished the effectiveness of time as a strategy.

- Resolution paths are diverging more sharply by asset quality and capital structure.

- Price discovery is emerging through selective transactions rather than broad based distress.

For much of the past two years, loan extensions and maturity modifications have limited forced sales across commercial real estate by deferring pricing decisions amid volatile rates and uneven fundamentals. However, this strategy is increasingly reaching its limits as higher for longer borrowing costs and slower income recovery reduce the value of delay.

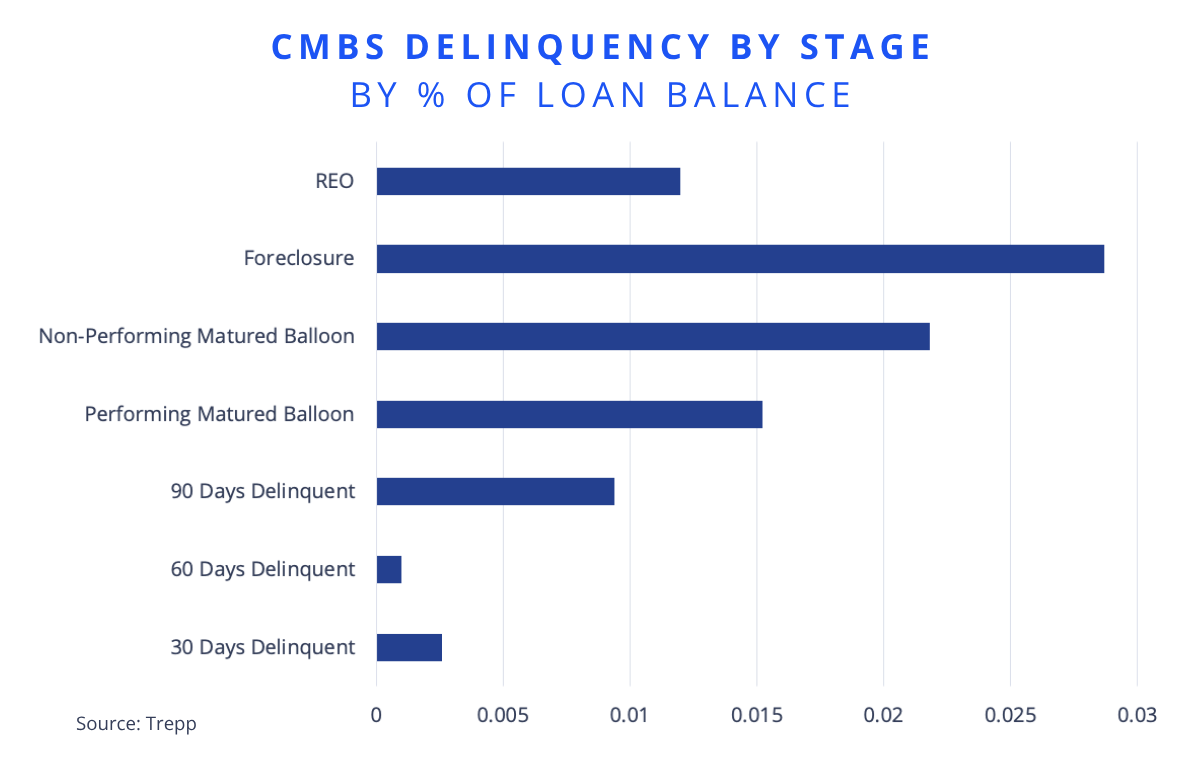

Current distress is concentrated in the resolution pipeline rather than in broad payment default. As of March 2026, performing matured balloon (1.5%) and non‑performing matured balloon (2.1%) loans together represent a meaningful market share, alongside foreclosure (2.8%) and REO (1.2%). Early‑stage delinquency buckets remain comparatively small. This composition is consistent with a market shifting away from repeated extensions and toward restructurings, recapitalizations, and selective sales as maturity events force pricing decisions.

Trepp data show that a substantial volume of outstanding loans, particularly within CMBS, has relied on extensions rather than refinancing or sale. Office assets account for a disproportionate share of these modifications. Many of these loans were originated in a materially lower‑rate environment, leaving capital structures misaligned with today’s debt costs even after multiple extensions.

Steig Seaward

Steig Seaward

Loan outcomes are more closely tied to maturity pressure than to payment default.

As those extensions roll off, lenders are becoming less willing to rely solely on time. Trepp’s refinancing analysis indicates that higher interest rates have materially reduced refinance proceeds, prompting lenders to require additional equity, pursue restructurings, or move toward asset sales as maturities are reached.

GlobeSt reporting suggests outcomes are now diverging more clearly. Assets with stable cash flow, manageable leverage, and realistic bases are finding paths forward through refinancing or recapitalization. Weaker assets are facing more constrained options, including deeper restructurings or enforcement actions. Importantly, this process has not produced widespread distress. Instead, transactions are occurring selectively, with pricing adjusted to current capital conditions.