- The absence of forward guidance shifts policy from pre-signaled to reactive.

- Rate volatility is likely to increase, especially at the short end of the curve.

- CRE borrowing costs will depend more on market pricing, with Fed commentary becoming one input among several.

- Fed commentary carries greater weight, but the signal is less unified.

- Investors will need to rely more on market-based proxies to read policy direction.

The Federal Reserve’s first meeting under Chair Kevin Warsh marks a shift in how monetary policy is communicated. By shortening statements and removing forward guidance, the Fed is emphasizing flexibility over a pre-signaled path, leaving markets to infer policy direction from data and dispersed Fed commentary. The result is a move from pre-communicated policy to market-interpreted policy, increasing volatility across rates, credit, and CRE capital markets.

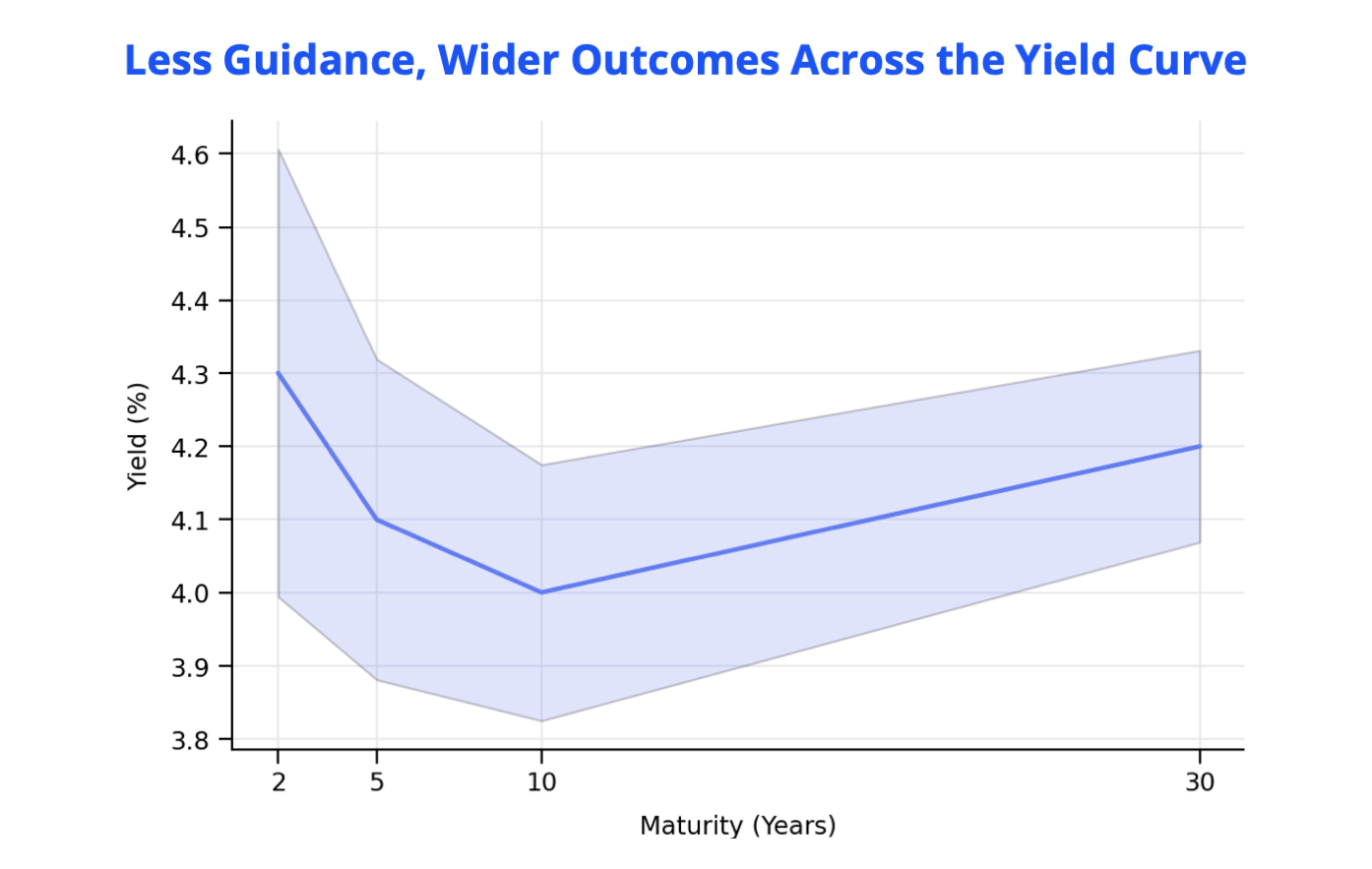

That uncertainty is translating into greater yield-curve volatility, especially at the short end, where market expectations for Fed policy are concentrated. The yield-curve framework shown above illustrates how that plays out across the curve: dispersion is widest at shorter maturities, where markets are most exposed to repricing risk. Further out on the curve, dispersion narrows but remains elevated, as long-term rates increasingly reflect inflation expectations, term premium, and broader macro uncertainty.

Steig Seaward

Steig Seaward

As forward guidance fades, short-term rates become more sensitive to changing expectations, making policy uncertainty harder to price.

With the Fed offering less explicit guidance, investors will need to rely on a broader set of signals to read policy direction:

| Signal | What to Watch |

| Hard Data | PCE inflation, employment, wage growth |

| Market curves | SOFR futures, Treasury term structure |

| Credit conditions | CMBS spreads, bank lending behavior |

| Fed commentary | Speeches, testimony, press conferences |

As policy signals become more dispersed across markets, each data release, curve move, and credit repricing becomes more consequential. In this environment, CRE capital markets will need to interpret Fed commentary alongside market-based signals to assess risk, price debt, and determine when liquidity can re-engage.