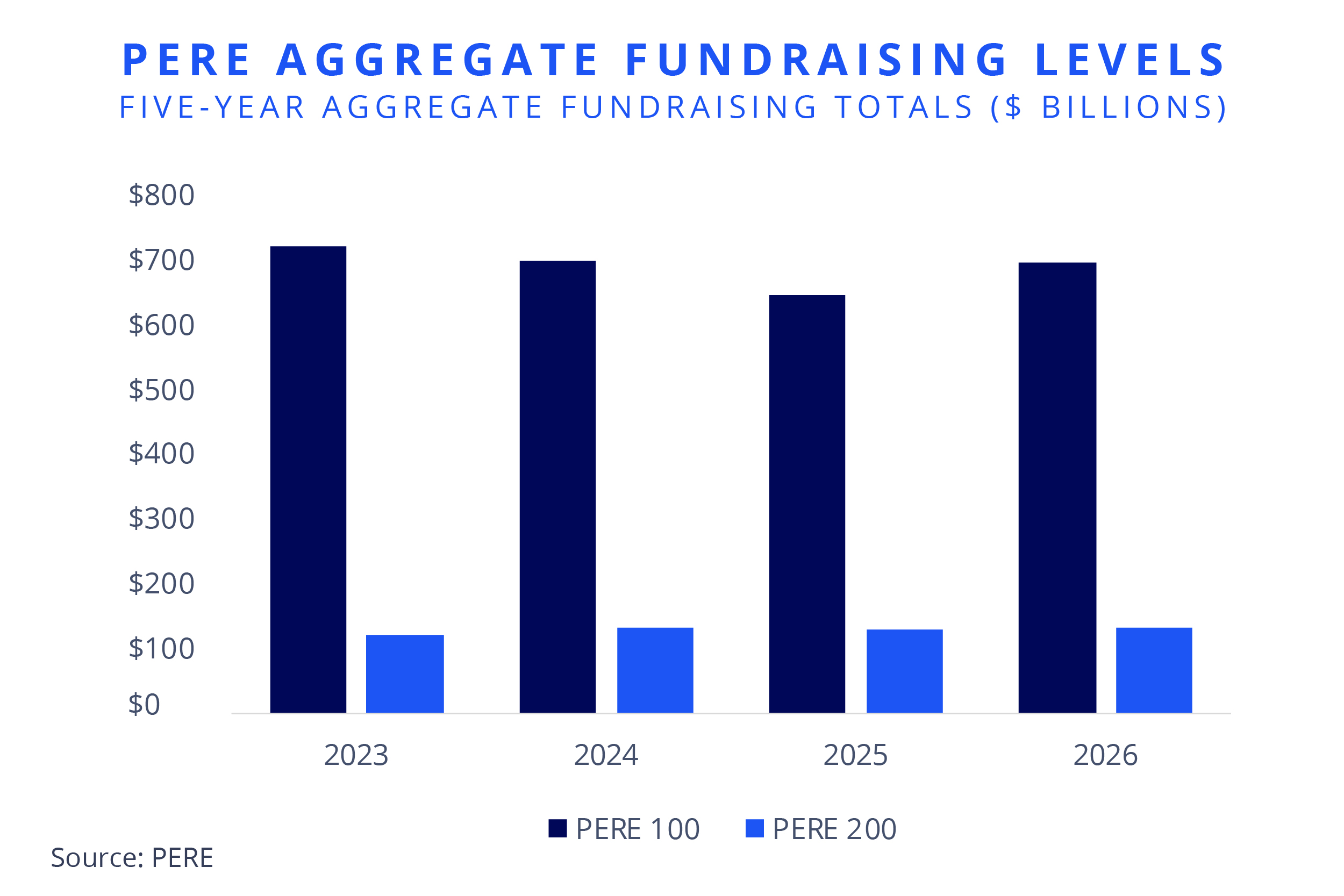

- PERE 100 capital rose year-over-year for the first time since 2023, adding $52 billion.

- Totals increased 8.1% to $698 billion, while the PERE 200 remained flat at ~$132 billion.

- Blue Owl and Ares drove ~$29.5 billion of growth, rapidly climbing the rankings, while legacy managers like Blackstone and Brookfield posted more modest gains in comparison.

- North America was the only region to post meaningful capital growth, while APAC, Europe, and other were largely flat.

Private real estate fundraising is stabilizing, with the 2026 rankings marking a turning point as the PERE 100 reverses a multiyear decline. Total capital raised increased year-over-year for the first time since 2023, with top managers adding $52 billion to their five-year totals as sentiment improves and capital begins to re-engage. The rebound, however, remains uneven and concentrated among the largest managers. Top-tier firms are gaining share while the broader manager universe, particularly the PERE 200, continues to face muted momentum.

The gap between the PERE 100 and PERE 200 continues to widen. The PERE 200 was effectively flat at ~$131.5 billion, reflecting limited fundraising momentum and ongoing challenges for smaller and mid-tier managers despite improving conditions.

Steig Seaward

Steig Seaward

Scaled alternative platforms are gaining share quickly, reshaping the competitive landscape while legacy leaders post more modest growth.

A key theme is the rapid rise of scaled alternative platforms. Blue Owl and Ares alone contributed nearly $30 billion in additional capital, far outpacing the ~$9.8 billion added by traditional leaders such as Blackstone and Brookfield. This reshuffling underscores investors’ growing preference for differentiated strategies and structures.

Geographically, the rebound is also concentrated. North American firms were the only cohort to see meaningful year-over-year gains, while Europe, APAC, and the rest of the world remained largely flat, highlighting continued U.S. dominance in attracting institutional capital.

Joe Fetterman

Joe Fetterman Jeffrey Myers

Jeffrey Myers David Burden

David Burden Frank Petz

Frank Petz